Life insurance and extreme sports have an interesting relationship. Though an individual might be entirely healthy and have no pre-existing health conditions, indulging in extreme sports means a high risk of an accident. Due to that, insurance companies look closely at each situation.

Examples of extreme sports include but are not limited to:

This article focuses on sky diving, its associated risks and what it means for life insurance companies and people who search for life insurance (including term life insurance, whole life insurance, and other life insurance types) while engaging in the sport of sky diving.

Though sky diving/parachute sports are considered an extreme sport, its safety standards and quality of gear have continuously improved over the decades. Nevertheless, there are some risks associated with sky diving – and insurance companies take good note of those risks. The risks include landing problems (late deployment, malfunctioning gear, potential collisions with other sky divers or objects, etc.).

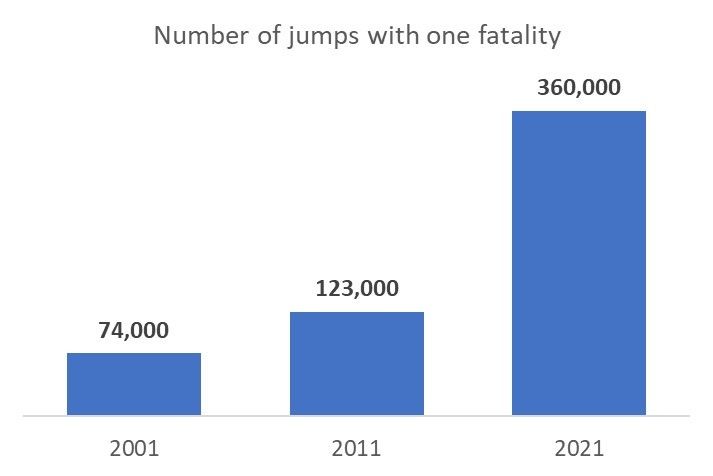

According to the United States Parachute Association, there were 10 skydiving fatalities in the U.S. in 2021 (per 3.57 mil jumps), meaning a fatalities rate of 0.28 per 100,000 jumps. That translates into 1 fatality per ~360,000 jumps. That is a 3-time improvement from 2011, which saw 1 fatality per ~123,000 jumps, and an almost 5 time improvement from 2001 with 1 fatality per ~74,000 jumps. (Source:)

Canadian numbers are not dissimilar. In 2014, the Canadian Sport Parachuting Association reported 1 fatality per 148,000 jumps.

It is important to mention that the risk varies if you are jumping solo or in a tandem with an experienced diver. In the latter case, risk decreases even further.

The quick answer is, it depends. There are several factors that impact your ability to get life insurance, such as:

For example, one of the life insurance companies we work with would charge standard rates for your life insurance policy as long as it is one jump and you have no intention to repeat it or become an avid sky diver.

Also, affiliation with a parachute or sky diving club results in standard rates as you will likely be exposed to high safety standards and surrounded by experienced divers.

There are some increased risk scenarios (e.g., intention to do repeated jumps) when a life insurance company will charge you an increased rate. For example, with one of our insurance provides, you’d pay $2.5 per thousand of coverage. That means that a $100,000 policy would cost you $250/annually or approximately $21/month. Should you decide to get a $500,000 policy, it would cost you $1,250/annually or around $104/month.

Should you engage frequently in high-risk jumps, your life insurance application is very likely to be declined.

In some cases, an insurer will issue a life insurance policy but will exclude your sky diving activity from potential claims. In this case, the policy pays out if a policy holder passes away from any other reason than sky diving.

In any case, should you answer a sky diving question positively, you will need to complete an additional sub-questionnaire explaining exactly your ski diving intentions.

Yes, sky diving does affect life insurance and you need to disclose it to an insurer when completing a life insurance application. Otherwise, any potential accident might not be covered.

Depending on your skydiving intentions, an insurance company will do one of the following:

In many cases, if it is just a low risk, one time jump (e.g., to try it out, in a tandem jump with an instructor), you have a great chance of getting a standard rated life insurance policy.

Nevertheless, you want to check with the insurance company to see if this risk is covered, while fully disclosing your intentions.

If you are interested in knowing “does life insurance pay if you die skydiving?” the answer is “it depends”. First of all, you need to understand if you already have an existing life insurance policy, or you are planning to get one before the jump.

If you already have a life insurance policy in place, you want to check the fine print. Review the full insurance booklet to understand if extreme sports and skydiving are covered. If an insurance broker helped you with the policy in the past, he/she can help you with this question. If your policy does not cover skydiving, you want to discuss this with your insurance broker/insurance company to find your potential options.

If you do not have a life insurance policy and plan to apply for life insurance while doing skydiving, you need to work with an insurance company that explicitly covers skydiving risks. You will need to complete a skydiving/parachute questionnaire and, if it is a low risk, one time jump, the chances are good that it will be covered. Make sure to confirm this via an insurance policy document or, if not available (i.e., skydiving is not explicitly included in the policy text) get a written statement from your insurance company/broker.

There are a variety of life insurance policies you can get when skydiving.

| Insurance Type | Medical Exam | Detailed Medical Questionnaire | Short Questionnaire | Coverage Limits | Important to Know |

| 1. Traditional, Medically Underwritten Life Insurance with STANDARD RATES | Yes | Yes | No | $5,000,000+ | Yes, for one jump and no intention to repeat. |

| 2. Traditional, Medically Underwritten Life Insurance WITHOUT A MEDICAL EXAM | No | Yes | No | $5,000,000+ | Yes, for one jump and no intention to repeat. You can avoid a medical exam if you fall into particular age segments and have good health without serious health-preconditions. |

| 3. Traditional, Medically Underwritten RATED Life Insurance | Yes | Yes | No | $5,000,000+ | Yes, in case of repeated jumps or some sky diving aspects increasing the risk of your jumps. |

| 4. Simplified Issue Life Insurance | No | No | Yes | $1,000,000+ | Yes, can typically qualify for this insurance. Questionnaires vary across providers. Most questionnaires will not ask you about extreme sports, but some may. |

| 5. Guaranteed Issued Life Insurance | No | No | No | $25,000+ | Yes, you can always qualify for this one. |

Pretty much every life insurance company offers life insurance for people who enjoy extreme sports, including Manulife, SSQ Life Insurance, Empire Life, Canada Life, Assumption Life and more. Treatment of extreme sports can vary from company to company.

We recommend working with an experienced life insurance broker who has access to most life insurance policies on the market and can compare application criteria for extreme sports and, skydiving/parachuting in particular, across a wide variety of insurance companies to get you the best rate and coverage.

Our experienced life insurance brokers are happy to assist you on this journey – simply complete the quote request on the right side of your screen.