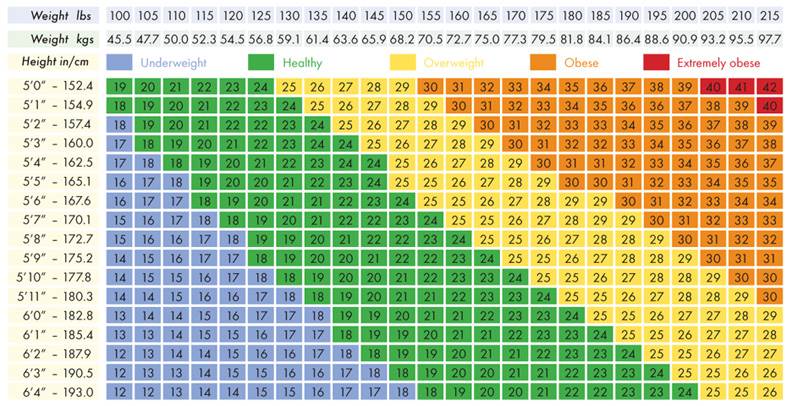

Body Mass Index (BMI) is a value that is calculated based on a few key metrics, such as your height and weight. This value is widely used in life insurance when calculating your physical condition and associated insurance rates.

The formula to calculate BMI (body mass index) is very simple: it is your weight in kilograms divided by your height in meters squared: BMI = Weight / (Height * Height)

Body Adiposity Index (BAI) is a value that is calculated based on a few parameters, such as your hip circumference and height. This value is widely used when estimating percentage of fat in a body.

The formula to calculate BAI (body adiposity index) is quite simple and empirical: it is your Hip Circumference in centimetres divided by your Height in meters in power of 1.5 minus 18: BAI = (Hip Circumference / (Height^1.5)-18

Source: FIRST NATIONS HEALTH AUTHORITY

Most insurers today are not using today the Body Adiposity Index (BAI). On a basic level all insurers rely on BMI. There would be a few reasons why it is the preferred measurement and thus more widely used:

That being said, an often misunderstood part about build ratings is that, when the information is available, many other factors can be considered to make a final decision.

Even more basic build calculators, like the one above, will now account for waist circumference when it is measured and available. For example, your BMI could be rateable +50, however having a smaller waist could reduce that rating to standard, whereas having a larger waist could increase that rating by another +25/+50. Quite often some favourable factors that can help an underwriter reduce a build rating (which is based on BMI), such as having no other rateable history and otherwise favourable cardiovascular risk factors (lipids, glucose metabolism, blood pressure, family history, etc). Typically, ”credits” will be available to reduce a rating by +25/+50.

Then there are the more complex ”cardiometabolic” calculators which outside of BMI will also account for data points such as: waist circumference, blood pressure, blood glucose, lipids, some cardiac biomarkers, liver enzymes, family history, alcohol use, smoking status, etc.

Each of these variables will either increase, decrease or have no impact on the final rating, so BMI is simply a starting point and from there numerous adjustments are made.

It is also worth noting that even companies that do not use cardiometabolic calculators are still considering a lot of data points before making a decision. The final rating is simply a bit less granular. Rather than making very slight adjustments for each variable, they look at each of them individually and only add together those the warrant a rating. If credits are available the underwriter would then assess if the final rating can be reduced or not.

It is worth noting that not all basic build or more complex cardiometabolic calculators use the same data points and attribute the same debits and credits to their equations. That means that a final decision can vary from one carrier to another, unless of course two companies use the same calculators and consider the same variables when they assess a client.

[…] For the purpose of this article let’s exclude big ticket items like paying off a mortgage or line of credit. For a full analysis of your insurance needs you can visit the attached link How Much Life Insurance Do You Need […]