Life insurance is one of the most widely used life and living benefits insurance products, but many questions remain about its tax implications. Understanding how taxes apply to life insurance is crucial, especially given the involvement of the Canada Revenue Agency (CRA).

Life insurance tax topics span various financial transactions:

As briefly mentioned above, there are two different policy types:

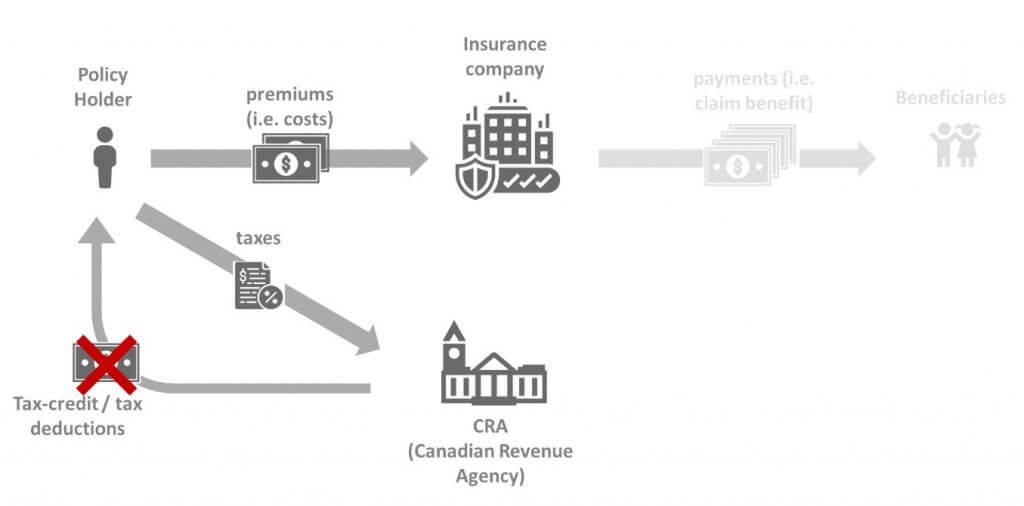

In the vast majority of cases, the answer to the question, “Are life insurance payments tax-deductible?” is no – life insurance premiums are NOT tax-deductible. An exception exists if a life insurance policy is used as collateral for an investment loan. In such instances, a portion of the premium may be deductible, but it’s crucial to tread carefully and seek professional advice.

The life insurance premiums that a person pays to an insurance company either on a monthly or annual basis are not tax deductible. Thus, there is no need to report this to CRA (Canadian Revenue Agency) in hopes of getting the premiums credited.

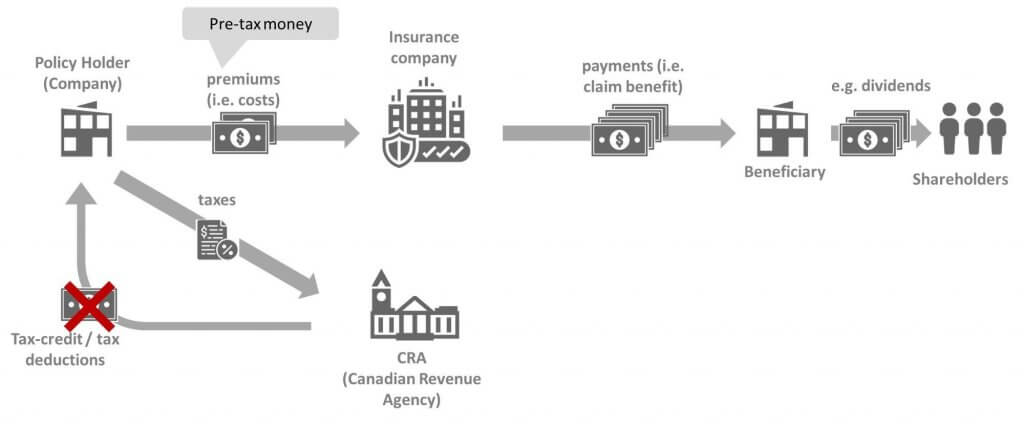

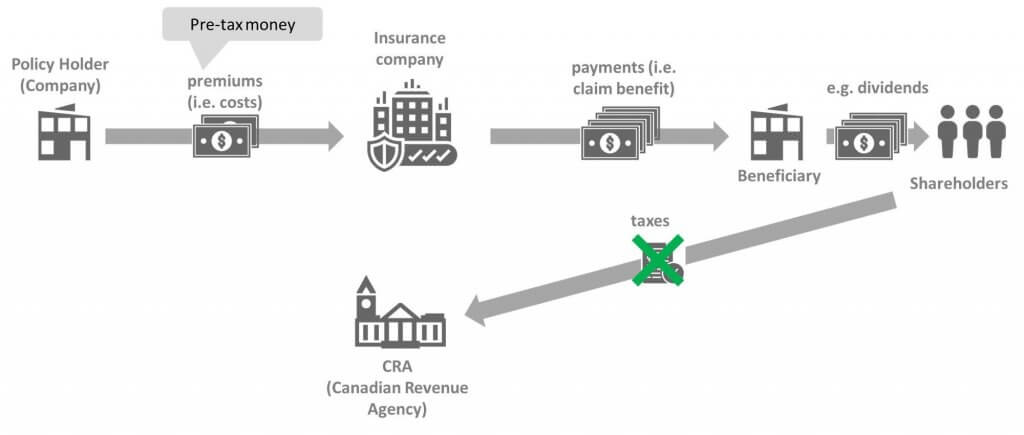

Corporate-owned life insurance premiums are not tax-deductible. However, if owned by a small business, corporate ownership can still be advantageous due to the difference between the small business and personal tax rates. A company gets to use lower tax dollars to pay for the life insurance premium.

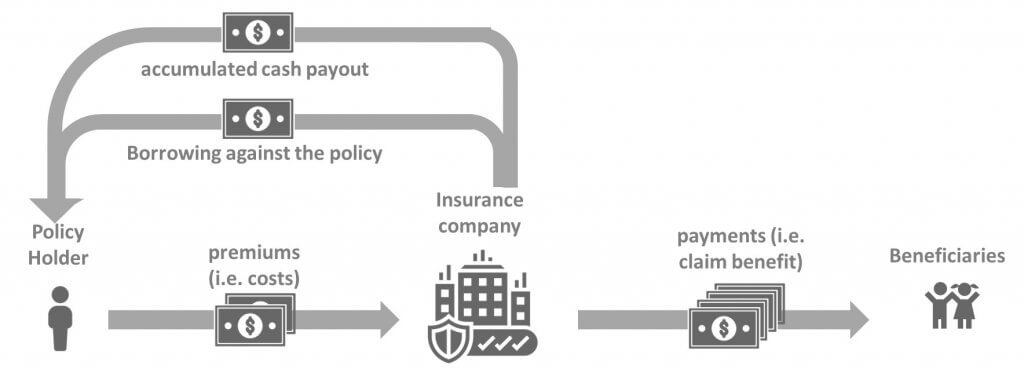

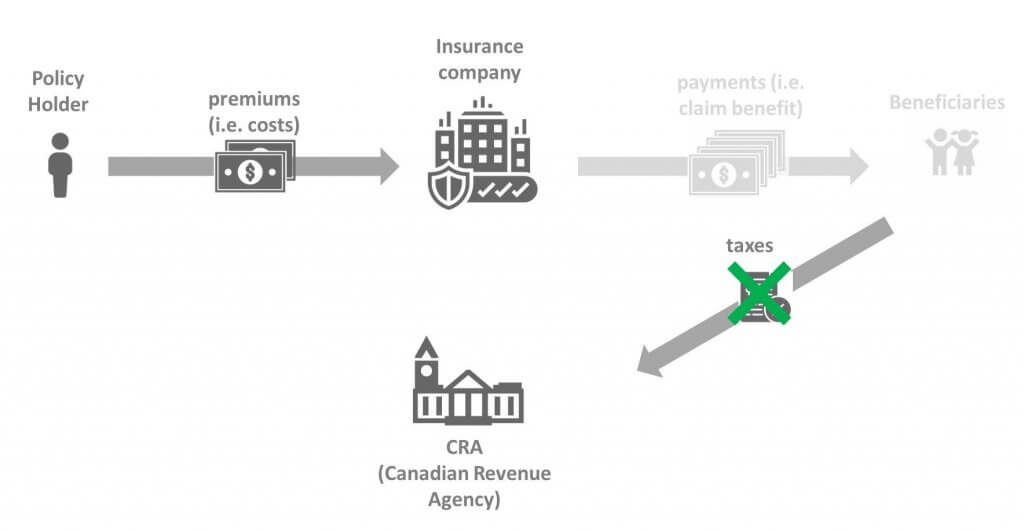

If a policyholder passes away, beneficiaries will receive the FULL claim payout. Life insurance proceeds are NOT taxable in Canada when it comes to claim payouts.

For example, if a policyholder had a $1,000,000 life insurance policy, their beneficiary would receive the entire $1,000,000 without paying taxes on it.

Proceeds from life insurance are not taxable (also called life insurance payments) and the beneficiary will receive the full benefit tax-free. Thus, CRA will not be getting a part of life insurance proceeds/claim payout.

When the beneficiary is a corporation, much of the death benefit will be able to be a dividend paid out to Canadian resident shareholders tax-free. An exception could be if a corporately owned policy (misguidedly) names a beneficiary other than the corporation. This causes tax problems.

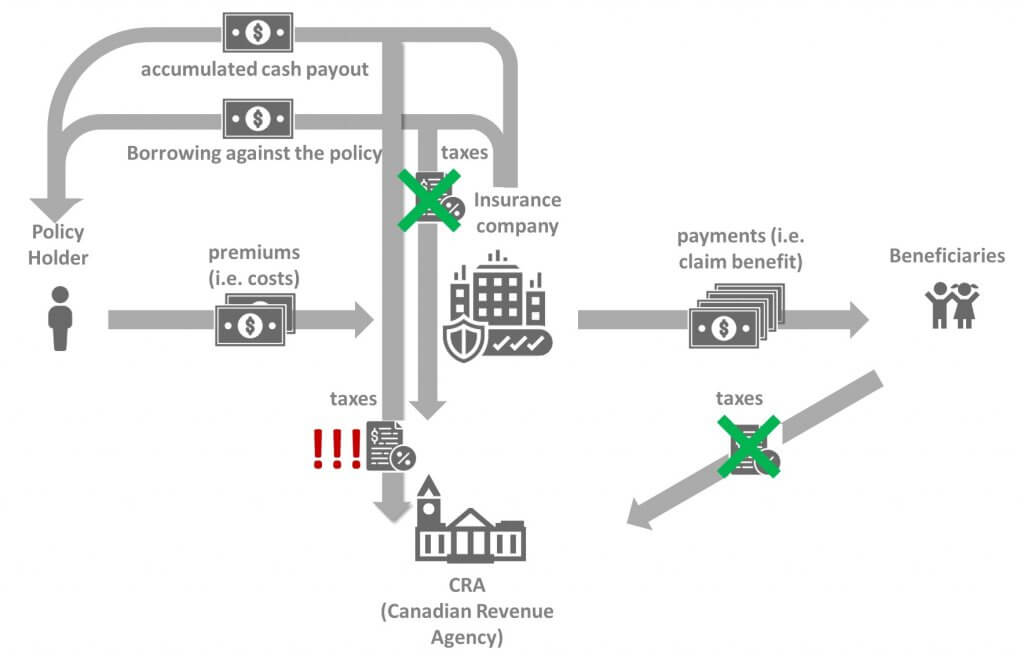

If you take out cash from your whole life insurance policy, there is often a tax to pay. For this reason, it is often better to take out a collateral loan against the policy. This is similar tax-wise to a line of credit against a rental property – no sale means no gain and no taxes. Upon death, the loan gets paid off by the death benefit and the beneficiaries get the balance. Note: the lender must be a third party (not a policy loan) for this to be onside with CRA.

Life insurance as a tax sheltering tool is another tax-related topic and there are numerous ways to use permanent life insurance (such as whole life insurance) for tax-savings purposes. We have a detailed article on this topic – Whole Life Insurance and Taxes: Everything You Must Know.

Also, our experienced life insurance brokers are happy to explain you the details of life insurance products and associated tax impacts. Simply complete the quote request on the right side of your screen.

Casey Cameron graduated from the University of British Columbia and has worked in financial services and insurance ever since.

He worked for six years with one of the world’s largest banks in Australia and Canada. After a stint in international banking, Casey spent a further six years with a boutique financial planning company in Vancouver, British Columbia and founded Camlife Financial in 2014.

He holds a professional financial planning designation and is a Fellow of the Canadian Securities Institute. Casey enjoys helping families, individuals and business owners with their financial planning, insurance and investment needs.