Insurance experts find some products more useful than others. For example: term life insurance, disability insurance, and critical illness insurance can change your life if you need the policy to pay out. However, mortgage insurance, accidental death insurance, and some other products fall into a category of “less useful products.” This is because a carefully constructed life insurance plan can eliminate the need for some policies. For example, let’s take a look at mortgage insurance.

Insurance experts find some products more useful than others. For example: term life insurance, disability insurance, and critical illness insurance can change your life if you need the policy to pay out. However, mortgage insurance, accidental death insurance, and some other products fall into a category of “less useful products.” This is because a carefully constructed life insurance plan can eliminate the need for some policies. For example, let’s take a look at mortgage insurance.

Mortgage insurance is offered by your bank to cover the cost of the mortgage, should one of the mortgage holders pass away. Some banks give clients the impression that they are required to purchase life insurance to protect a mortgage. They are already protected by the mortgage itself, and according to the Financial Consumer Agency of Canada, banks are explicitly prohibited from coercively “tying” the sale of one bank product with another.

Download here a guidance from Financial Consumer Agency of Canada (as a PDF).

Did you know that a term or permanent policy that you may already have in play can cover the requirement? (And it could be less expensive and have better terms too.)

Why is this? Let’s take a closer look.

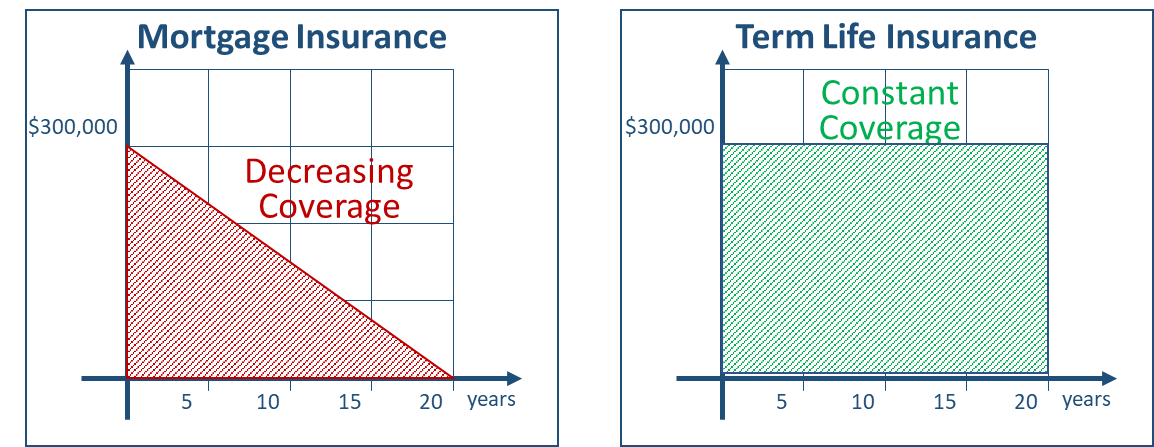

Look at the visual below. The mortgage insurance offered by a lending institution (bank), per its definition, covers only an outstanding mortgage amount. This amount could be $300,000 in the first month, as per illustration below.

But as time passes by, the coverage becomes smaller and smaller as you pay off parts of your mortgage (see the left part of the chart below). Your mortgage insurance premiums do not change, though. As an alternative to mortgage insurance, a simple term life insurance, also shown on the chart, will preserve its full coverage through the entire life of the policy. With mortgage insurance, over time, you pay more for less.

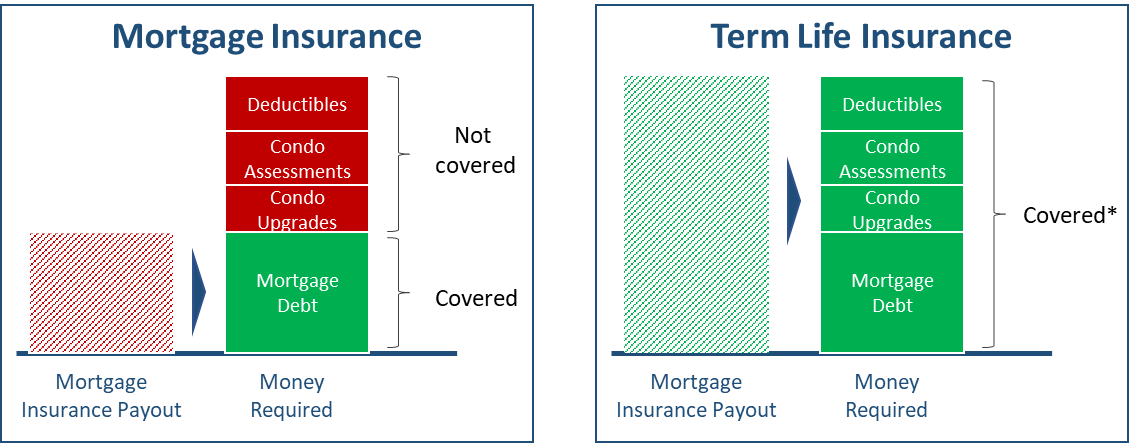

When people think about getting mortgage insurance, they are purely focused on the mortgage, but there are many other home ownership aspects that might drain your money should you not be prepared.

One of them is home upgrades/repairs. These might be required throughout your entire property ownership. No mortgage insurance policy covers maintenance expenditures for your home.

Another important aspect, especially when dealing with condos, are condo assessments and condo deductibles. These are cases where a condominium board runs out of reserve fund money to make necessary upgrades, repairs, or to pay a required insurance deductible in the case of a larger claim. When this happens, condo owners get a “special assessment.” These costs can add up to several thousands of dollars per condo unit and must be paid no matter what. Condo reviews for condos in Toronto, condos in Mississauga, and other locations provide insights into these little-known aspects of condo ownership.

Mortgage insurance will not leave you enough coverage for those items because it only covers outstanding mortgage debt. Term life insurance, on the contrary, could have enough room to cover all these potential issues.

If your partner does not have a high income on his/her own and there is no income loss protection in place, they might have to sell the property to survive.

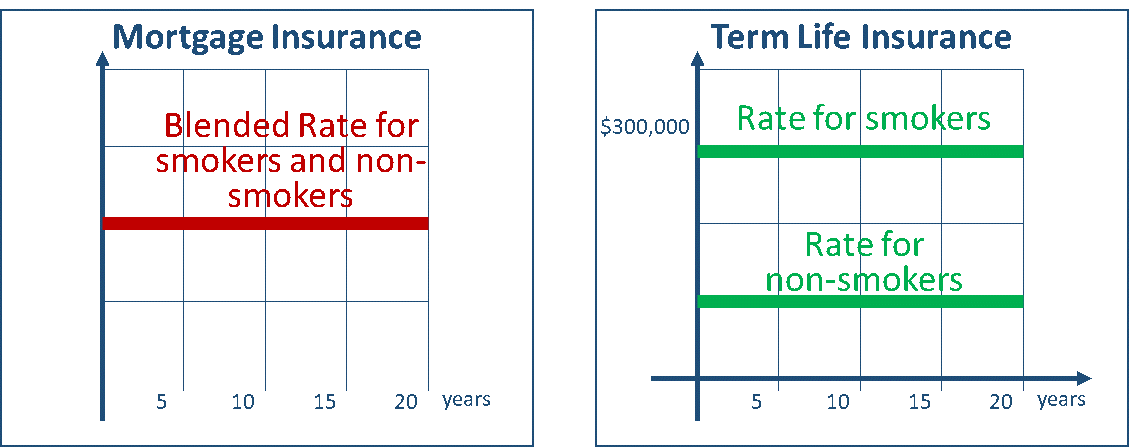

You will often find that mortgage insurance rates are higher than rates for the identical coverage offered via term life insurance. The reason is that, in most cases, insurers lump together rates for both smokers and non-smokers. That allows them to sell insurance and estimate rates much faster, but on the flip side, all non-smokers pay more.

A standard term life insurance policy considers your health and habits and rewards non-smokers with better rates, as illustrated below. Whole life insurance and universal life insurance will typically have higher rates than term life insurance, but they come with additional benefits and cover policyholders throughout their entire life.

Life insurance expert Richard Parkinson suggests that, if an insured person is in excellent health, he/she can benefit from discounts of up to 25 percent, which is a very significant amount. A lending institution will not take into account your health when selling you a mortgage insurance policy.

It is not surprising that, in the case of mortgage insurance, the beneficiary is the bank since mortgage insurance only covers the outstanding mortgage balance. However, a term insurance payout goes directly to your beneficiaries, such as to your family members and loved ones, who are free to decide to use the money for multiple purposes: continue to pay the mortgage payment and use the cash for other purposes such college tuition fees, move to a different location, etc.

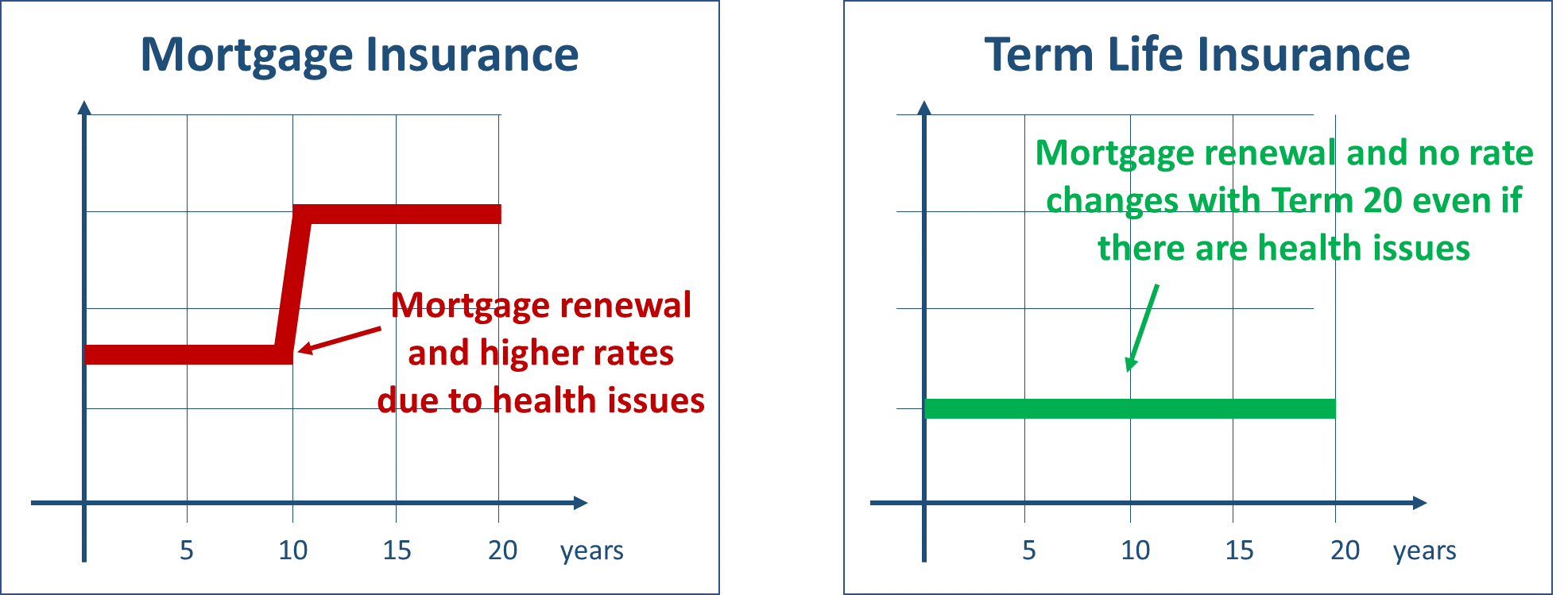

As Richard Parkinson points out, it is typical to change lenders at renewal, but mortgage insurance provided by a bank or any other lending institution is not transferrable. This means you need to get a new policy with your next lender, and that could potentially increase your costs. The graphic below illustrates what can happen. As the worst case, you could become uninsurable, negating the opportunity to take advantage of a better mortgage rate.

A term life insurance policy will stay with you for the entire period of its validity (20 years in this example as a Term 20 life insurance policy) without changes in rates.

The nice thing that often makes people buy mortgage insurance is how easy it is to get it – it often comes with no medical exams or tests if a mortgage amount is low. But everything comes at a cost! Having no medical exams means that an insurer accepts higher risks and thus charges you more for them. It is important to know though that many banks will ask for a paramedical exam for coverages over $250,000. You, as a customer, will pay in the meantime and then 3-4 months later they can tell you that you are declined.

Several years ago, the CBC Martketwatch program presented an expose of mortgage insurance from banks and bank’s record was not good. You can see this CBC video about bank mortgage insurance here.

Standard term life insurance comes with a simple medical exam that allows the insurer to provide you with better rates. If you want to make sure that you are not overpaying for the coverage, in most cases, it is a better way to go.

We hope you found these mortgage insurance insights helpful. Should you look for optimal ways to protect your property and insure that your family does not carry a mortgage burden if something were to happen to one of the bread winners, contact us today; our life insurance specialists will help you with mortgage insurance alternatives.