The world today is not the same as it was 30 years ago. That is why some of the questions insurance clients are asking deal with the realities of this complicated world. One of these questions relates to life insurance and terrorism, and how insurance companies treat these cases. In fact, there are several scenarios, and it is important to understand all of them. Also, it is important to understand that, while some companies deal with this topic differently than others, the key principles are still the same.

The world today is not the same as it was 30 years ago. That is why some of the questions insurance clients are asking deal with the realities of this complicated world. One of these questions relates to life insurance and terrorism, and how insurance companies treat these cases. In fact, there are several scenarios, and it is important to understand all of them. Also, it is important to understand that, while some companies deal with this topic differently than others, the key principles are still the same.

Acts of terrorism can hit anywhere – no country is exempt. How would insurance companies treat a situation when a policyholder did not travel at all or traveled to a country that is considered safe and still became a victim of terrorism?

In this case, most Canadians are covered by their policy and a claim will be paid in full.

Here is what an insurance representative said: “If someone were to die because of a terrorist attack and had no involvement in it whatsoever in Canada, then the claim will be paid.”

The situation is different if a policyholder travelled to a dangerous location and became a victim of terrorism there. In this case, insurance companies may deny the claim because they see this risk as preventable because it was a policyholder’s decision to travel to a dangerous location.

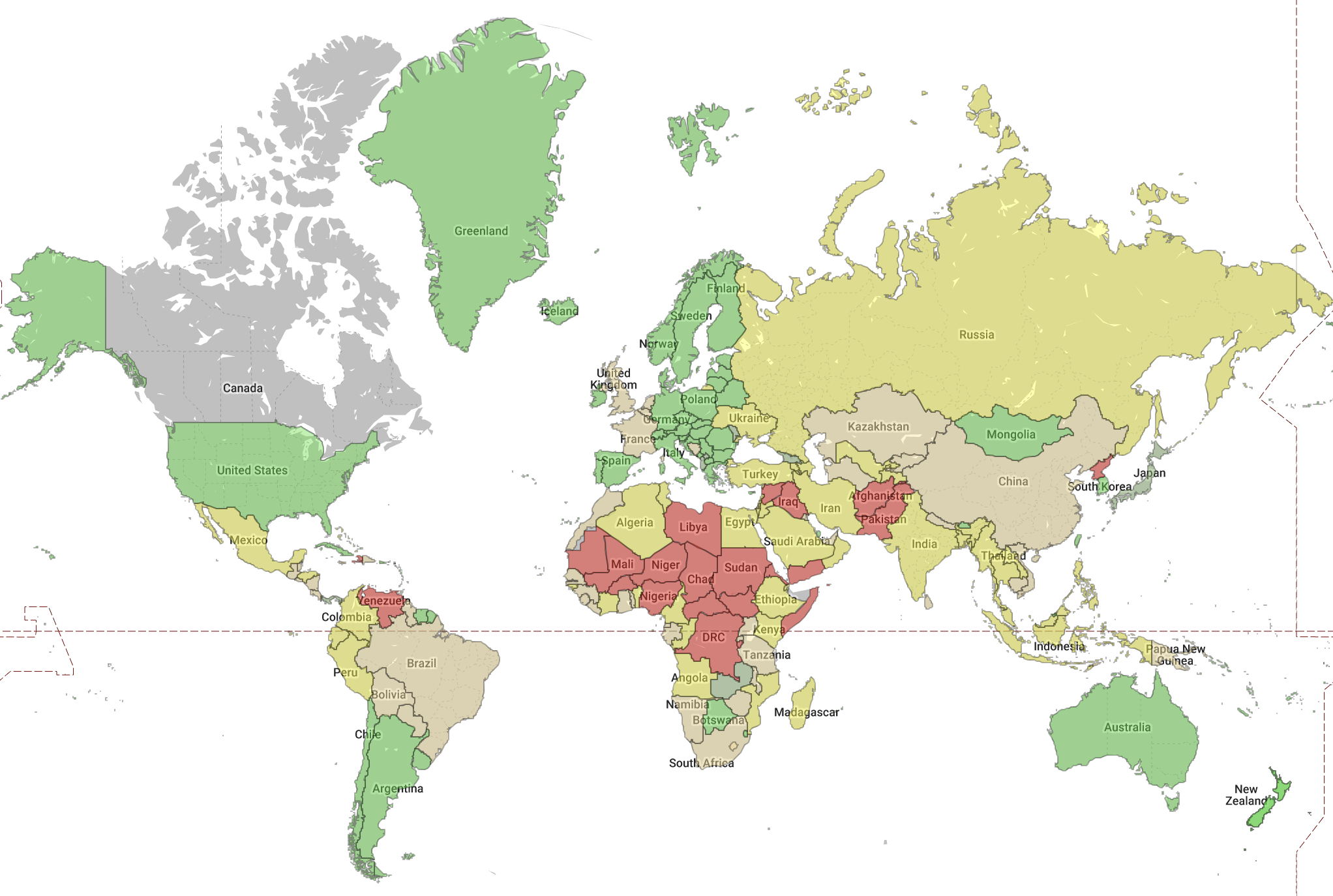

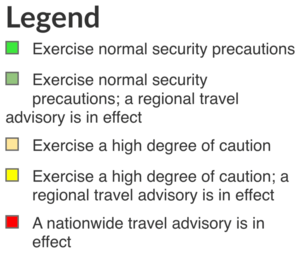

insurance companies define regions, countries, and destinations as dangerous when a government advisory was issued. This list is constantly updated by the Government of Canada and can be found here: Travel Advice and Advisory.

The Government of Canada uses the following classification:

The information below was released on September 10, 2019 by the Government of Canada.

Here is what insurers say about this situation: “If a person is travelling and dies due to an act of terrorism and there was a government travel advisory to that region/country/destination, the claim may be denied.”

Interestingly, insurance companies treat four destination categories differently. In many cases though, the first two categories, “Avoid all travel”- and “Avoid non-essential travel”-countries, will be either declined or will require an exclusion (meaning that a claim will not be paid). In some case, your planned length of stay may determine a type of policy that you can qualify for.

Please note that some types of life insurance policies, e.g. Simplified Issue Life Insurance, might not have travel questions at all.

This scenario is quite obvious – in this case, a life insurance claim will be clearly denied. The insurance companies say, “If a person dies due to a terrorist attack and participated in the terrorism act, the claim will be denied.”

Riots are included in the same category, and anybody who died participating in a riot would not be covered either.

An accidental death rider is an additional feature of a life insurance policy that, when purchased, typically increases the amount of the claim payout. For example, if a policyholder has a $500,000 life insurance policy with an accidental death rider that doubles the death benefit, and then the insured passed away in a plane crash, the life insurance beneficiaries will receive $1,000,000.

The situation looks different in the case of a terrorist attack – a number of insurance companies do not see it as an accident similar to a plane or car crash; thus, only basic life insurance coverage will be paid, not the part of the accidental death rider. It means, in an example above, if the plane suffered a terrorist attack and the insured died, the beneficiaries will receive only $500,000.

We hope that this provides you with helpful information for buying life insurance, but we also hope that you and your loved ones will never face the scenario of being a victim of terrorism.

If this is a major concern for you, please make sure to read the sample policy contract before you buy a policy, and get an authoritative reply from an authorized representative of the life insurance company.