Every business owner is familiar with the old saying, cash is king. When you have it on hand, cash provides stability and the capacity for growth when opportunities arise. Since cash is the lifeblood of any business, shareholders struggle when it isn’t close by. Frankly, many view the purchase of life insurance as a threat to that cash flow, even when an accountant recommends it. However, there is a way to have your cake and eat it too using an insurance strategy called the immediate financing arrangement or IFA for short.

Every business owner is familiar with the old saying, cash is king. When you have it on hand, cash provides stability and the capacity for growth when opportunities arise. Since cash is the lifeblood of any business, shareholders struggle when it isn’t close by. Frankly, many view the purchase of life insurance as a threat to that cash flow, even when an accountant recommends it. However, there is a way to have your cake and eat it too using an insurance strategy called the immediate financing arrangement or IFA for short.

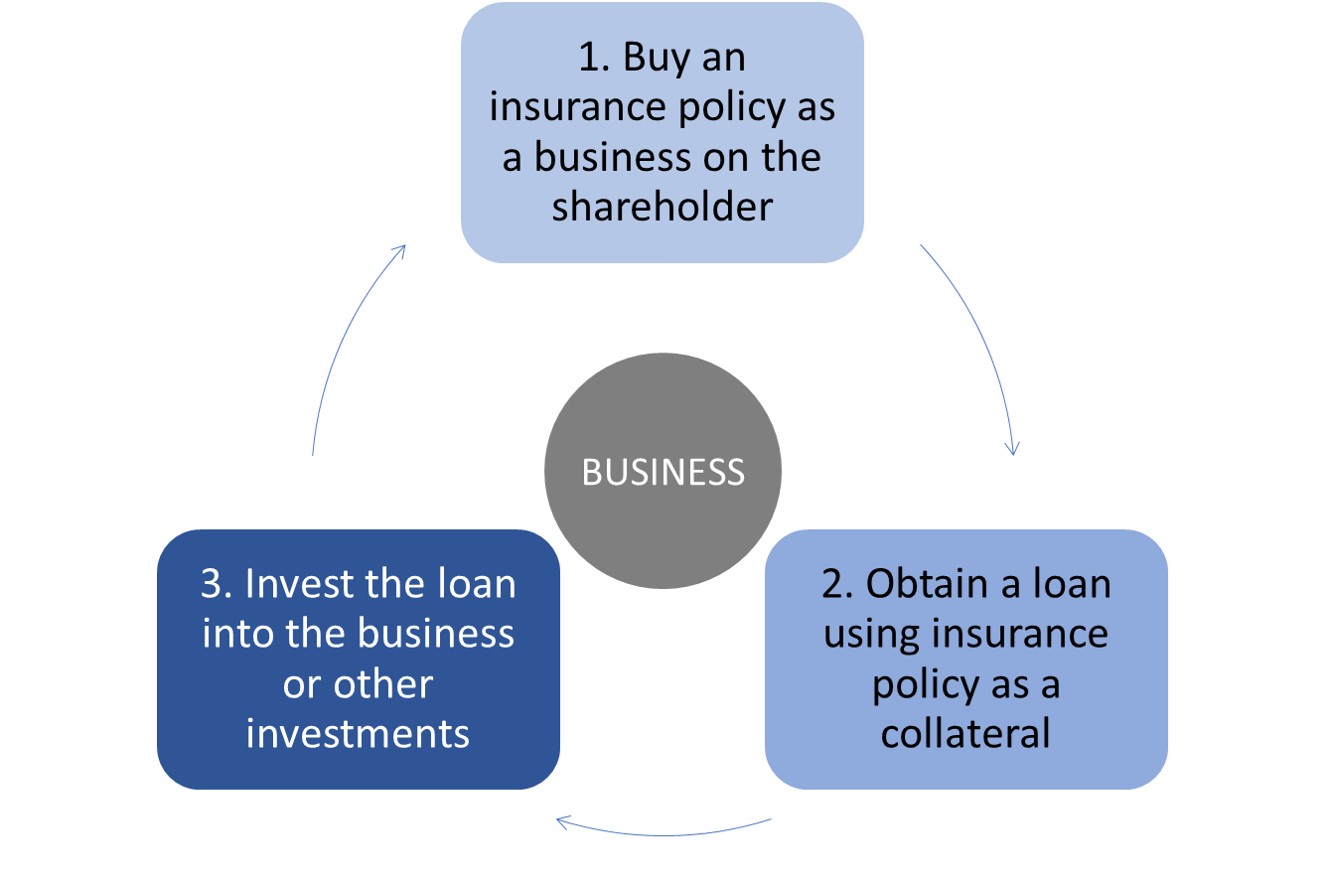

In a nutshell, IFA allows a business to finance a life insurance premium on behalf of a shareholder, create tax deductions and ultimately transfer assets tax free from the business to the shareholder’s estate. It uses a life insurance policy with a cash accumulation component.

It is important to know that a business can purchase an insurance policy on the life of a shareholder. Accountants usually recommend this since premiums can be paid with lower-taxed corporate dollars compared to higher-taxed personal dollars. The tax savings become significant when purchasing an insurance policy that builds cash value. Put simply, cash value is like equity in owning real estate in that it is more expensive than renting but provides you with longer term value.

Unfortunately, there is still a tax loss in this scenario since premiums are paid post corporate tax unless some planning is done to recover cash flow. The solution involves borrowing money from a bank or financial institution and using the insurance policy as collateral for a loan. Then, the loan can be invested into the business or other investments if the business does not require all of the cash flow for operations immediately.

Here are the key implementation steps of an IFA strategy:

If you already have an insurance policy with cash value, you may be able to use it instead of taking out a brand new one. Please note that a term life insurance policy does not accumulate cash and thus cannot be used for this strategy. You should also remember that to obtain an insurance policy, the insurance company may require medical evidence and will always require financial evidence.

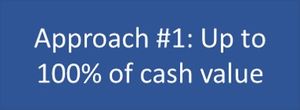

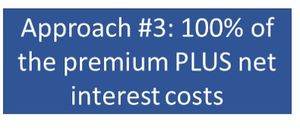

There are three main ways to design an IFA. Let’s have a look at them in detail.

The first is to provide the loan based on the cash value of the insurance policy. It is common for the loan to range from 75%-90% of the cash value, but some lenders will go up to 100%.

Often, the cash value is initially less than the premium paid by the business, so there is still a cash outlay. Therefore, the second approach is to lend the entire premium to the business. However, this will require additional collateral for the loan, which can be investments, real estate, or other assets.

The third approach does not actually have any cash flow leakage at all as the premium and yearly net interest costs are advanced. Thus, your internal rate of return is limitless. It’s also possible to structure a personal IFA, but is typically done within a business structure.

Banks and financial institutions have different documentation requirements, rates, and terms. Some are very streamlined and can do smaller cases where premiums are as low as $10K per year. On the flip side, larger cases where the premium is $250K or more can take a bit longer to arrange, but can secure rates lower than Banker’s Acceptance (BA) rates. If the business does not want a floating rate, it can also structure a fixed rate loan, although this is less common.

We had previously mentioned the business paying premiums with lower-taxed corporate dollars. Additionally, there are two potential tax deductions provided when properly structuring the plan that ultimately help reduce the overall costs of the insurance.

As with all investment strategies, there is a list of potential scenarios to consider. Not all of them will be realized but they should be understood by you and your accountant, and properly disclosed. This way you can determine if the strategy remains relevant and appropriate for the right reasons.

If the loan rate is higher than the credited rate, extra collateral may be required by the bank or financial institution. If extra collateral cannot be provided, the bank may require a withdrawal of a portion of the cash value, which will trigger a taxable gain that is included into income at 100%. The taxable gain is calculated as the amount of cash value that is over the adjusted costs basis or ACB. The insurance company will provide the ACB at any point in time.

Yes, there is actually a lot of flexibility in terms of the policy, the loan, and your commitment to it. It is important for businesses to be able to pivot when challenges arise.

My favorite part is designing the policy itself. Of course, there is always a base amount of premium required but you can also create the capacity for additional deposits, which help you achieve higher cash values in the early years. Additional deposits build the cash value dollar for dollar right away, resulting in less collateral security requirements from the bank or financial institution. However, since the additional deposits are optional, the business can tailor the premium stream to match the evolving business.

The loan itself is usually not set in stone. If desired the loan can be paid down at a faster rate through regular payments, lump sums, or even in full as cash becomes available. There is no penalty to pay off floating rate loans or they can be switched into fixed terms if requested.

As mentioned earlier, the shareholder should document, in advance, the direction of pay procedures to ensure that there are no shareholder benefit issues.

After the loan is paid, there may still be some residual insurance proceeds. These funds can remain within the business or be paid out tax free to the shareholder’s estate. The mechanism that allows this tax-free payment is called the capital dividend account (CDA). The CDA balance is calculated as the death benefit minus the adjusted costs basis. The remaining CDA balance within the business after paying off the loan can be distributed to the deceased shareholder’s estate or the remaining shareholders while alive by using other business assets.

The true value of this is substantial and should not be underestimated. It can be measured by combining the yearly tax savings of the asset if it had remained within the business and the tax cost to normally move an asset from the business to an individual. The IFA strategy can be designed specifically to optimize the release of trapped retained earnings and business assets tax free.

The remaining insurance proceeds can also be used to fund buy/sell agreements, replace the shareholder, redeem shares, or pay off business debt.

The immediate financing arrangement can lower the net cost of life insurance premiums for a business owner so that cash is kept on hand. The overall rates of return on the strategy are potentially infinite as cash flow is not hampered. There is a way to have your cake and eat it too, and the best part is that you don’t have to share any with Canada Revenue Agency.

Interested in talking about life insurance solutions that can help you and your organization? Our insurance professionals look forward to hearing from you.

Author’s Background:

Author’s Background:Steve Meldrum is a contrarian by nature. He is the corporate insurance specialist at Swell Private Wealth, a boutique firm specializing in corporate tax strategies for medical and dental professionals. His advisory practice also supports quarterly training for national and regional accounting firms, lawyers, and private bankers on advanced insurance strategies. Established as a thought leader for the dual advisor approach, he consults other financial advisors in collaborative planning. He loves the challenge of solving complex problems in creative ways with a mantra that simplicity brings clarity.