The topic of interest rates impacts numerous aspects of daily life. While the interest rates in Canada have been low for over a decade, last year Canadians saw unprecedented rate increases, reaching levels last seen in 2008.

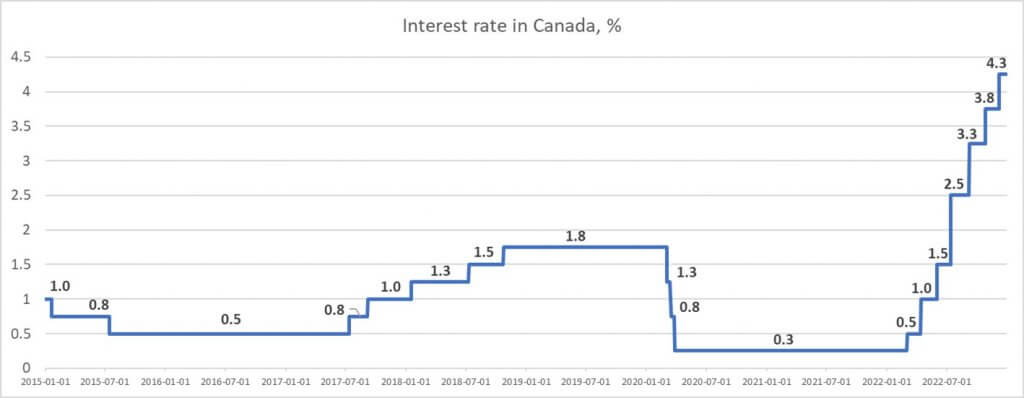

The chart below illustrates the evolution of the interest rates between January 2015 and January 2023. While interest varied between 0.5% and 1.8% between January 2015 and July 2022, rates skyrocketed to 4.3% by the end of 2022.

Interest rates affect real estate affordability and the cost of borrowing money. For example, over the past year both fixed and variable mortgage rates have increased between 3% and 4% respectively, with the most current rates sitting between 4.99% and 5.99%.

With the Bank of Canada increasing interest rates throughout 2022, Canadians have seen a sizable change in both the amount of mortgage they can qualify for as well as the monthly payments associated with their mortgage.

The increased interest has caused the average mortgage payment to grow between 45% and 60%, and the amount a purchaser can borrow to decrease by about 38% year over year, which has been one of the main drivers forcing housing prices lower.

Here are two scenarios to put these numbers in perspective when comparing changes in monthly mortgage payments and the amounts a Canadian household can borrow as of the beginning versus the end of last year.

| Scenario | Beginning of 2022 | End of 2022 | Change |

| Scenario 1 | Mortgage: $400,00 (25-year amortization) Monthly payment: $1,692 | Mortgage: $400,00 (25-year amortization) Monthly payment: $2,556 | Monthly payment increase: +51% |

| Scenario 2 | Household earning $100,000 annually. Can be approved for $600,000-mortgage. Monthly payment: $2,142 | Household earning $100,000 annually. Can be approved for $500,000-mortgage. Monthly payment: $2,745 | Decrease in the amount of mortgage to qualify for: -20% Monthly payment increase (normalized for $100K): +54% |

The first example above demonstrates that an increase in rates has caused the average mortgage payment to increase between 45% and 60%. For a mortgage of $400,000 with a 25-year amortization, the payment is up to $2,556 from $1,692 a year earlier.

From the second example above, we see that a Canadian household earning $100,000 annually (with some assumed home ownership expenses) could have been approved for an approximate $600,000 mortgage with payments of $2142/monthly in the beginning of the last year. This same household, in December 2022, is looking at an approximate $500,000 mortgage approval with payments of $2,745/monthly.

This is a 20% drop in the amount of mortgage a Canadian can qualify for, which translates into 20% less they can spend on a home.

Currently, we are in very unique times with short-term bond yields (and mortgage rates) being higher than 5-year terms. Historically, variable rates have provided better savings compared to fixed rates, both in rate and mortgage exit penalties.

Consumers, however, should always select an interest rate based on their risk tolerance and goals, as 2022 has shown us that we are not immune to rapid rate increases. Current market conditions at the time of obtaining a new mortgage or renewing must also be factored into the decision process. In December 2022, variable rates were higher than fixed rates, making fixed rates more attractive.

Some forecasters believe fixed rates are at their peak, so to lock into today’s rates for 5 years is not attractive to many. Additionally, with talks that the Bank of Canada could lower rates at the end of 2023, there may be a good opportunity for lower rates in the next 12 to 24 months. Consumers are strongly encouraged to consider shorter terms (1- to 3-year fixed rates) to keep the opportunity open to obtain a lower rate when rates come down again.

Every person’s situation is unique; it is wise for consumers to seek independent advice on the best mortgage product for their needs.

About authors:

We thank both Shawn Stillman from Mortgage Outlet Inc. and Armando Cuccione from ApproveU.ca for their exceptional insights.

|  |

| Shawn Stillman, CPA, CA Mortgage Broker/ Co-Founder Mortgage Outlet Inc | Armando Cuccione Mortgage Consultant Founder of ApproveU.ca |