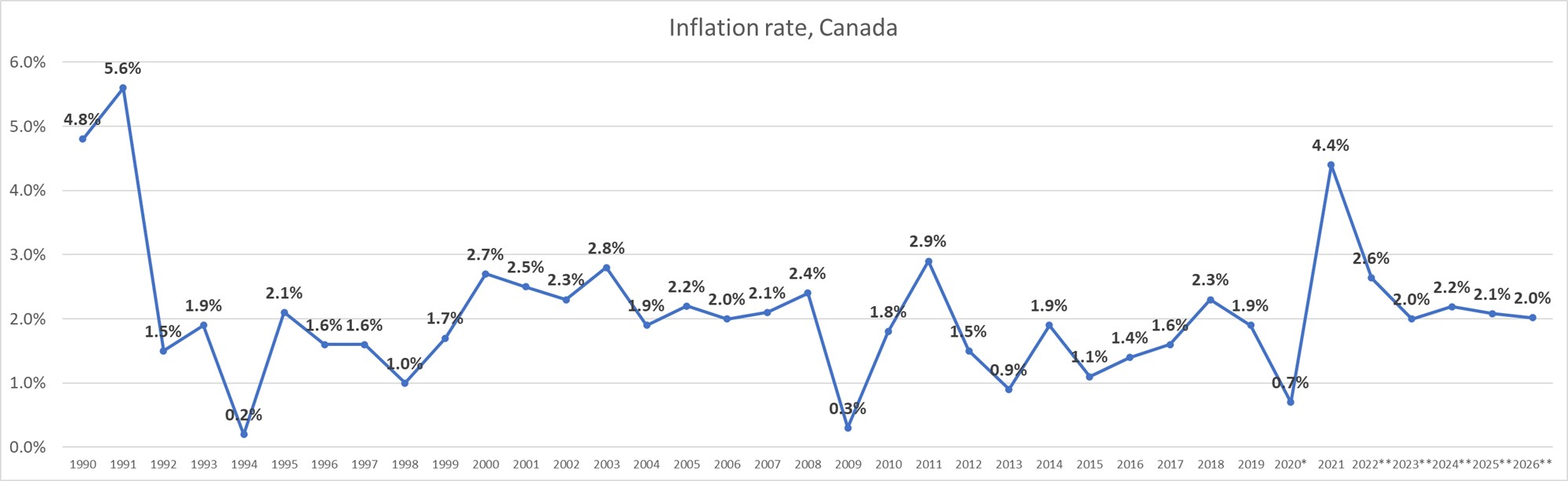

The pandemic has changed our life over the course of the last two years. It has impacted every industry; some more than others like travel and restaurants, some less such as software and professional services. It has also had a huge impact on our society and macro-economic metrics. One such metric is inflation, which has been increasing significantly in 2021, reaching 4.4% (see the graph below). The last inflation peaks took place in 1990 (4.8%) and 1991 (5.6%). Inflation tends to swing, on average, between 0.2% and 2.9%.

Today we will discuss the theme of increased inflation and how it affects life insurance rates, given that inflation strongly correlates with interest rates and impacts insurance in a number of ways. We asked several insurance industry and thought leaders to share their perspectives.

Click on the thought leader’s picture below to explore their perspective.

We have seen the rise of inflationary pressures lately with the pandemic and the breaking of the supply chain. Those pressures were expected to be temporary, but they now seem more likely to last longer and require the intervention of central banks by increasing their policy interest rate. Early intervention of central banks will likely be successful in maintaining inflation within the Bank of Canada’s target range of 1% to 3%, so we do not expect inflation to impact insurance rates significantly.

If not contained, however, a higher inflation rate could result in increased costs for insurance companies, which could, in turn, reflect on insurance product rates. On the other side, this effect might be mitigated if the inflation pressures result in a sustainable increase in interest rates.

I would say that inflation makes the need for planning for your retirement or insurance even more important as savings today need to meet the needs of tomorrow. Higher inflation increases the amount of insurance you will need to enable your children/dependants to maintain their standard of living.

Universal Life Insurance (UL) is well positioned to help someone with that planning. For life insurance, equity returns often outperform inflation (way more than bonds) and a well-funded UL Level (face plus fund) policy could provide an opportunity to have the certainty of the face amount of insurance, while covering the increasing cost of the standard of living through the accumulation available from the equity investment.

The other consideration is that high inflation may increase the future cost of the same insurance, as expenses assumed in pricing would increase. Not what anyone wants to hear: “Get it now as the cost may increase…”

Inflation factors into the pricing/profitability analysis in two primary ways:

1. Maintenance Expenses: Companies do need to price for future expenses and higher inflation will mean that cost components will increase. Although it depends on the product, maintenance expenses are generally a small portion of the overall ‘cost’ of a life insurance product, so upward pressure on prices due to this would be relatively modest.

2. Expected investment income: As inflation goes up, there can be an expectation that interest rates will rise and that can mean that assets supporting any reserves during the life of the policy will generate more investment income and that can improve profitability and potentially support lower prices. The level of assets supporting any reserves depends greatly on the type of product with 10-year term having little build-up, while permanent products would have the most. Since most life products are paid for with recurring premiums over their lives, the company would have to be confident that any interest rate increases driven by the higher inflation would be sustained since the assets are generally bought over time.

It should be added that if expected inflation is expected to increase in a sustained way, then clients may need to buy larger face amounts as the value of the death benefit over time would erode due to inflation (e.g. if a client wants to ensure the death benefit would be sufficient to cover a child’s university tuition in the future). As such, that increase in face amount could offset the lower premium rate from higher inflation-driven interest rates; however, it does depend on what is driving a client’s insurance needs.

I think the real impact of inflation will be reflected in interest rates beginning to rise. There is no direct correlation between inflation and insurance pricing, but there definitely is a HUGE correlation between interest rates and insurance pricing.

As a result, I think the impact of inflation will have an effect on insurance pricing, but we will only see it over the medium-term, and it will be most notable in products that have long-guaranteed premium durations. (Term 100, level universal life policies, T75 & T100 critical illness insurance contracts to name a few…)

Inherently, insurance companies are investment companies. Investing premiums received before the need to pay claims form a significant part of their profitability. As the nature of these investments needs to be conservative to support their ongoing obligations, interest rates on government grade bonds (or equivalents) drives much of the yields insurance companies can chase. When interest rates are low, insurance companies must gather more premiums to receive the same amount of returns. This explains the sharp increase in level UL & T75/T100 CI pricing when the bank of Canada slashed interest rates in the beginning of COVID.

Once inflation kicks in, there is a short lag and then banks must increase interest rates. As rates rise, the pressure on insurance companies to gather premiums is lowered as they can get more yield on less premium dollars being received. As the market is quite competitive, insurance companies aren’t afraid to lower premiums, assuming they can still support their profit requirements. An environment where inflation is happening – rates are increasing, and long-term stability of those forces seems realistic – is perfect for a softening of insurance pricing, specifically on contracts with long-guaranteed premium durations.

We only foresee a temporary increase of interest rates for 2022 and a return to similarly low rates for 2023 and beyond. Though CPI is higher than the upper bracket set by the Central Bank, the significant indebtedness created by the federal government to support the economy during the COVID-19 pandemic is just too high for the federal government to allow a higher interest rate environment. The current term structure of interest rates reflects this same perception (its low and relatively flat).

Impact on life insurance premium rates: There is an inconsistency between CPI (Consumer Price Index) and the interest rates. CPI being higher than the current term rate structure, it implies that it will cost more to administer a policy than it did in the past. Therefore, there will be pressure on premium rates to slightly increase, but competition among insurers will probably push the premium down to maintain them at a similar level as the current one.

Inflation won’t have much, if any, direct impact on life insurance. The expenses of running/ administering policies by the insurance companies is the item in their pricing that is most directly affected by inflation. Although this will be affected, this is one of the smallest costs that they cover in pricing of insurance products.

The indirect impact will be more significant.

Low interest rates have had a significant impact on life insurance products. Today’s low interest rates are exerting downward pressure on par policy dividend scales across the industry.

However, if higher inflation leads to higher interest rates, as has historically been the case, such higher interest rates will lessen the downward pressure on dividend scales. That’s why showing current dividend projections to clients is very misleading. We always show current dividend -1% and it’s even more safe to illustrate at -1.5%. Nobody likes surprises.

Low interest rates have also been a leading cause of the increase in level cost of insurance rates in universal life products. Higher interest rates may, in time, lead to lower-level COI rates although this would take some time to occur (i.e. interest rates would need to increase by at least a few percentage points and be stable at those higher levels for a period of time before they would affect COI rates).

For consumers, inflation will impact the cost of goods and the things on which we spend our money. Therefore, advisors will need to review their clients’ overall lifestyle needs and likely adjust their needs analysis to include impact of inflation.

Remember when interest rates were at 10%? We did illustrations back in the day suggesting clients could invest $1M of insurance death proceeds at 10% and earn $100k per year before tax. Clearly this was not sustainable as interest rates tanked and we have had to lower expectations quite a bit over the years and look at increasing amounts of insurance needed to keep up with interest. Same may hold true with inflation but the question is, for how long?

Given the current climate, I do feel that inflation will continue to rise moderately over the next while as the economy attempts to get back to a sense of “normal.” Despite this being the case, I’m not sure I see an increase in life insurance rates in Canada due to a couple of factors.

As inflation is generally accompanied by an increase in interest rates helping life insurance carriers in a number of areas which is positive, something to consider is also the issue for consumers in budgeting life insurance premiums as part of their overall monthly spend when they are financially pressured. It’s going to be difficult for a number of policyholders to make ends meet for a number of essential items and unfortunately, often times life insurance premiums are at the greatest risk of being eliminated. With this being the case, an increase in premiums would most likely hinder the amount of new sales and policyholders, which is something the industry wants to avoid, leading to rates holding steady for the near future.