Universal Life Insurance gives you flexible, cost-effective coverage that lasts a lifetime. It can be personalized to suit your changing needs and has a combined tax-advantage investment component that you can manage according to your risk tolerance and financial goals.

Universal Life Insurance gives you flexible, cost-effective coverage that lasts a lifetime. It can be personalized to suit your changing needs and has a combined tax-advantage investment component that you can manage according to your risk tolerance and financial goals.

Universal Life Insurance allows you to adjust your premium payments (reasonable limits apply) as your needs or situation change.

Thus, three key features of this life insurance are:

Ability to change your regular premiums (unlike whole life insurance)

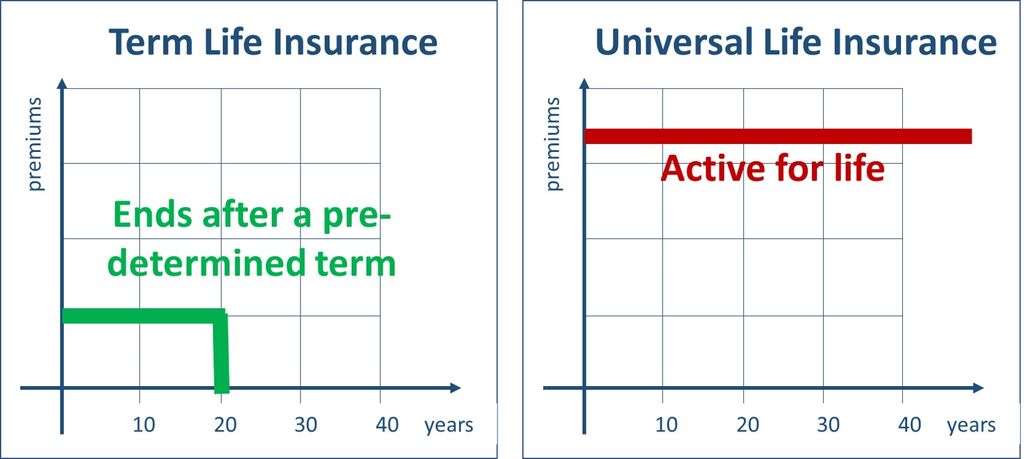

It is the ideal choice for people interested in flexible coverage. Unlike term insurance, which covers for a set number of years, universal coverage protects your family for life, as long as you keep up with the premium payments giving you permanent coverage.

The policy has an investment component that gives you the opportunity to grow your wealth, so you have the option of using your life insurance while you are still alive. This means you can fund financial goals or leave more to your beneficiaries.

All the premium payments you make go into a policy fund. This fund pays for the cost of your coverage plus investments. The balance remaining after coverage costs are invested on a tax-advantaged basis. There are a variety of investment options for you to choose from, based on your risk tolerance and financial objectives.

How much your investment will grow depends on the performance of your investments and the amount of your premiums. The money in the investment portion of your account is yours. You can use it to make premium payments or a source of savings. You can use it as collateral for a loan, withdraw it outright or just let it grow for financial security for your loved ones. Don’t forget that borrowing or withdrawing funds from your policy reduces its cash value.

An overview below summarizes both positive and negative aspects of Universal Life Insurance

|

Pros of Universal Life Insurance |

Cons of Universal Life Insurance |

|

|

Here are a few examples of universal life insurance quotes generated as of September 2018. Please note that numbers can strongly vary based on personal profile of each applicant.

| Male, 35 years old, non-smoker |

Female, 35 years old, non-smoker |

|

|

Coverage: |

Starting at $69.33/month |

Starting at $60.83/month |

| Coverage: $200,000 |

Starting at $129.07/month |

Starting at $113.15/month |

| Coverage: $500,000 |

Starting at $293.54/month |

Starting at $250.92/month |

Interested in this insurance? Our brokers can help you with Universal Life Insurance quotes

A Universal Insurance policy can be very complicated. There are so many options and variables that the average person prefers a straight-forward term policy – or so is the common belief.

Sales of universal life insurance (annualized premiums) dropped by 24% in Q2 2017, compared to Q1 of 2017. Yet in the first half of 2017, they were up 6%. Universal Life Sales sales totalled ~$62,000,000 in Q2, 2017.

Thanks Michael. Agreed understanding what your buying is key. Many consumers got a great deal on Universal Life Policies, especially those Canadian consumers that locked in to Level Cost of Insurance plan before the recent rate hikes among Canadian carriers. But the key is to know what your buying and if you unsure get your answer in writing.

“The policies themselves can be very confusing even for certain brokers. So if you are investigating a Universal Life policy make sure you are working with a broker who understands how the policies work.”

I couldn’t agree more. Even when explained properly, many consumers are completely unaware of what they’re getting into. I frequently speak to new clients who tell me horror stories of their policies about to lapse or lapsing – they were completely blindsided.