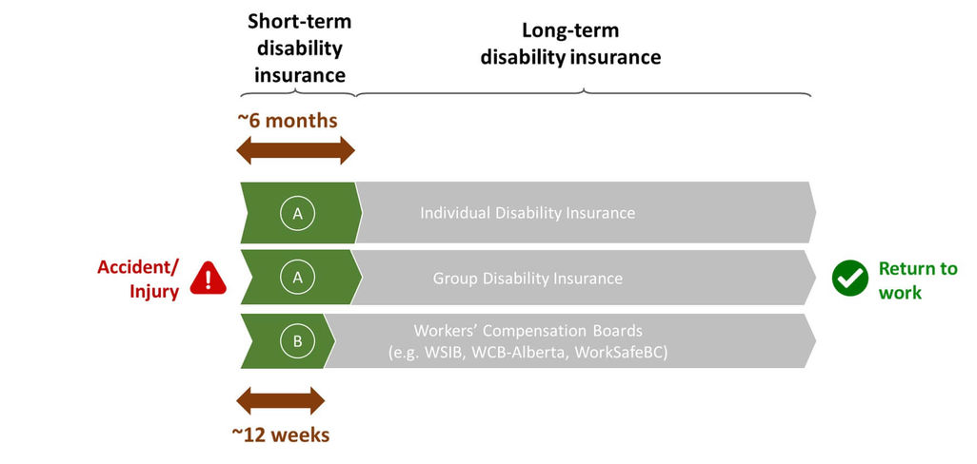

Disability insurance helps protect your income when you cannot work due to an accident and some forms of illness. Short-term disability payments help fill the gap between the incident and either your return to work or your switch to long-term disability benefits. Short-term policies are available under group (work or association sponsored coverage), or as individual policies, as well as from Workers’ Compensation Boards (note that e.g. WSIB only covers work-related incidents). Most major carriers in Canada sell short-term disability insurance coverage including but not limited to: Manulife, Sun Life, Canada Life and Industrial Alliance. The chart below details how short and long-term coverage works in Canada.

Short-term disability insurance activates a few days after the proper verification of your disability. This can take one to seven days. The typical payout period is six months.

Your short-term disability payments are only tax free if you pay the entire amount of the premium, such as with an individual policy. If your employer provides this coverage through their group plan and pays all or part of the premium on your behalf, your benefit will be subject to income tax.

The premium for short-term disability insurance varies as this coverage is tied to your classification of occupation. Other factors that influence the premium include your health, lifestyle, age, and coverage cap as set by the individual carrier. Even within carriers, coverage and premiums can vary among their products. Disability insurance can be complicated to set up; always use the services of a broker to ensure you are getting the best product for your situation and budget.

Unlike long-term disability insurance, short-term disability insurance starts just a few days after the verification of your incident. It lasts for around six months (or less if you can return to work sooner). After the benefit period ends, if you are unable to return to work the benefit may switch over to long-term coverage (providing you meet the criteria and you have the coverage already set up to activate). Do not be surprised (or alarmed) if the insurance company conducts another assessment after your short-term coverage ends as they will seek ways to help you recover faster. Your case may also be transferred to a long-term case manager.

|

Similar to individual coverage, your case under group coverage kicks in after a few days, and lasts for around six months before being converted, if necessary, to long-term. You may be subject to another assessment and receive a long-term disability case manager. Not all group coverage includes short-term disability coverage, however, as the company may rely on your accessing EI for what would have been the short-term coverage span. Group plans pay between approximately 45%-85% of your income – and it is very important to note that no matter where you get your coverage (group or individual) you will not be able to collect more than 85% of your gross income. In addition to group coverage being on the lower end of the coverage cap that is dictated by your occupation class, carriers also cap the amount you can receive monthly. You cannot stack policies from different sources to gain more than 85% of your income, but you can have more than one policy in place if you want to top up your coverage. Further note that the definition of disability can change after two years of a claim to “any reasonable occupation,” which means you are expected to work at any job you can handle, even if it is a different career or industry (or salary/wage) than before your disability. Group plans end when you leave your employer or the association. There may be a limited time opportunity to switch to individual coverage without a medical. If leaving your employer or association, talk to the plan administrator about this option. |

Expert tip from Lorne Marr “Short-term disability is generally offered as part of a group insurance policy. It usually pays a percentage of pre-disability earnings on a weekly basis. The percentage of income covered can vary. Benefits often range from 50% to 100% of your weekly earnings. And depending on the group plan benefits can be higher in the first 6 weeks, reducing in subsequent weeks.” |

Similar to individual coverage, your case under group coverage kicks in after a few days, and lasts for around six months before being converted, if necessary, to long-term. You may be subject to another assessment and receive a long-term disability case manager.

Not all group coverage includes short-term disability coverage, however, as the company may rely on your accessing EI for what would have been the short-term coverage span.

Group plans pay between approximately 45%-85% of your income – and it is very important to note that no matter where you get your coverage (group or individual) you will not be able to collect more than 85% of your gross income. In addition to group coverage being on the lower end of the coverage cap that is dictated by your occupation class, carriers also cap the amount you can receive monthly. You cannot stack policies from different sources to gain more than 85% of your income, but you can have more than one policy in place if you want to top up your coverage.

Further note that the definition of disability can change after two years of a claim to “any reasonable occupation,” which means you are expected to work at any job you can handle, even if it is a different career or industry (or salary/wage) than before your disability.

Group plans end when you leave your employer or the association. There may be a limited time opportunity to switch to individual coverage without a medical. If leaving your employer or association, talk to the plan administrator about this option.

“Short-term disability is generally offered as part of a group insurance policy. It usually pays a percentage of pre-disability earnings on a weekly basis. The percentage of income covered can vary.

Benefits often range from 50% to 100% of your weekly earnings. And depending on the group plan benefits can be higher in the first 6 weeks, reducing in subsequent weeks.”

Short-term disability coverage is very important for self-employed individuals that do not have income protection if they become sick or have an accident. You may also qualify for Canada Protection Plan-D (Canada Protection Plan disability benefits) because you contribute to Canada Protection Plan as a self-employed worker. If you are low income, you may have access to provincial programs, such as ODSP. You can also access EI sickness benefits, but only if you have paid into the program.

Most major carriers in Canada have disability coverage as a standalone product or as part of their other plans. For example, Manulife has both disability insurance and a combination product called Synergy ® that combines life, critical illness, and disability insurance.

One of the best ways to help inform your decisions about financial products is to read honest, independent consumer reviews. InsurEye has collected reviews since 2012 and has a free database of disability insurance reviews for you to explore.

Short-term disability insurance can be purchased through agents, brokers, directly from carriers, and even online. This policy should be structured to dovetail with either EI or long-term benefits, and since there are regulations around occupation class and which one your career fits under, we strongly recommend talking to a broker. Unlike an agent, a broker works with several carriers. They are compensated by the insurance companies, so you can use their services for free. They are also not limited in how many Canadian carriers they can work with, so they have access to a wide range of policies and applications that they will review on your behalf. Brokers are personal shoppers for insurance.

Many factors influence your short-term disability quote, as seen in the overview below. After reviewing these factors, complete a form and click the button on the top of this page to get a quote.

Benefits as a percentage of income: Benefits are limited to between around 45%-85% of your income, and this depends on your occupation class. You cannot stack policies to receive more than your regulated allowance.

Benefits cap: The insurer caps how much you can collect as a benefit per month. For example, if you earn $9,000/month, your benefits may be capped at $5,000/month. If your employer pays the premium, you must pay taxes on the benefit. If you pay the premium, the benefit is tax free.

Length of benefits: Short-term benefits end after about six months. You are expected to return to work as soon as possible.

Waiting period: Also known as the elimination period, the waiting period is the time between your approval and when your benefits start. Short-term benefits start quickly, but long-term benefits can take up to 90 days to kick in. Always have some money in an emergency fund to help you handle the elimination period, and the difference between your benefits and non-benefit income.

Pregnancy is not considered a disability, but complications arising from pregnancy may allow you to go on short-term disability benefits. It will all come down to what your insurance carrier allows under the policy. For example, being ordered by your doctor onto bed rest may or may not be covered. If you are pregnant or planning to be, contact your group plan sponsor or your agent/carrier/broker and together, go over the details so you know exactly what to expect from your coverage should your pregnancy have unfortunate complications.