Getting hurt on the job or becoming too ill to go to work for an extended period of time means losing your income. Disability insurance is coverage designed to protect a portion of your income against this risk. It pays a share of your income for a set amount of time, or until you recover (whichever period is shorter).

There are two types of disability insurance: short-term and long-term. Short-term comes first (usually about six months) and then, if required, long-term can start after.

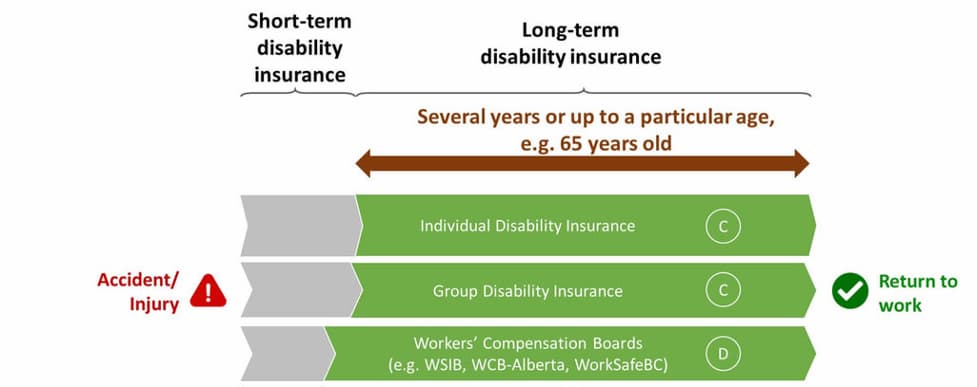

Long-term disability insurance is available for individuals, through group (association or employee sponsored) benefits, or through WSIB coverage. In some cases, the coverage can last for years, or even until your retirement.

Long-term disability starts once your short-term disability coverage, which is usually six months, runs out. Coverage is provided through an individual policy, a group policy, or through Workers’ Compensation Boards coverage (e.g. WSIB). While it is possible to have more than one long-term disability policy in place, they all work together to ensure not more than approximately 85% of your income is replaced. This is to discourage fraudulent use of the system.

The graphic below explains the relationship between short and long term disability:

Most situations fall into three categories that will determine how long the benefit will last:

These limits vary among insurers, and even among the policies carried by the same insurers.

Basically, long-term disability insurance covers income lost due to an injury, accident, and some forms of illness (read the policy carefully to know which illnesses are covered, and the determining criteria for the severity of the illness).

It’s important to note, however, that different styles of disability insurance cover different situations. For example, WSIB only covers work-related incidents, but private individual insurance covers incidences that occur on or off the job.

Disability insurance payments from all sources cannot exceed 85% per cent of pre-disability income. This is to prevent fraud. Even then, do not expect that you can layer policies up to the 85%. Depending on your occupation class and the nature of your policy, payments range from a maximum of 40%-85%. If you are receiving payments from a variety of sources, some will be reduced to accommodate your maximum coverage allowance.

When working with a professional to set up your disability insurance, focus on enough coverage for your ongoing necessary expense and debt. Some budget tweaks may be required should there be a gap in the allowance and your expenses.

Your long-term disability payments are only tax free if you pay the entire amount of the premium, such as with an individual policy. If your employer provides this coverage through their group plan and pays all or part of the premium on your behalf, your benefit will be subject to income tax.

The term individual long-term disability insurance refers to the policy you buy on your own – not a policy from your employer as part of their benefit package. Many carriers offer individual long-term disability insurance, including but not limited to: Manulife, Sun Life, Canada Life, and Desjardins Insurance.

|

The term group long-term disability refers to a policy sponsored by an employer or association (such as AMA or your university’s alumni association). Group coverage ends when you leave your employer or association. There is, on most group policies, a limited timeframe where you can convert the coverage to an individual policy. In many cases you can do this without a medical exam, so if you need to do a conversion, make sure you do so promptly. |

Expert tip from Lorne Marr “When getting a long-term disability insurance policy, it is very important to understand the definition of disability within your policy. For example, many group plans offer a “Regular Occupation” definition for the first two years of the plan, and then switch to an “Any Occupation” definition. An “Any Occupation” disability insurance classification is the least liberal, and, generally, the least expensive, type of disability insurance.” |

The term group long-term disability refers to a policy sponsored by an employer or association (such as AMA or your university’s alumni association). Group coverage ends when you leave your employer or association. There is, on most group policies, a limited timeframe where you can convert the coverage to an individual policy. In many cases you can do this without a medical exam, so if you need to do a conversion, make sure you do so promptly.

“When getting a long-term disability insurance policy, it is very important to understand the definition of disability within your policy.

For example, many group plans offer a “Regular Occupation” definition for the first two years of the plan, and then switch to an “Any Occupation” definition. An “Any Occupation” disability insurance classification is the least liberal, and, generally, the least expensive, type of disability insurance.”

There are several options for disability insurance for the self-employed. You can purchase your own policy, and you may qualify for Canada Protection Plan-D (Canada Protection Plan disability benefits) if you have contributed to Canada Protection Plan as a self-employed worker. Low-income self-employed individuals may qualify for program such as ODSP. EI sickness benefits are also an option, but only if you have paid into the program.

Yes, long-term disability insurance is worth it. Even if only 40% of your income is covered, that is 40% of your expenses for food, debt repayment, and bills. Disability insurance is used as part of your overall budget and financial planning. Also ensure you have other applicable coverage in place (critical illness, life insurance, auto insurance) and strive to build some cash in a savings account to help offset expenses while unable to work.

Most major carriers offer long-term disability insurance as a standalone policy or as part of a package. For example, Manulife offers standalone disability policies, as well as Synergy® which combines life, critical illness, and disability protection into one convenient product.

Long-term disability insurance premiums are extremely varied because several factors determine the cost. First, based on your occupation class, a determination is made of how much of your income can be replaced. It may be as low as 40% or as high as 85%. There will also be a benefits cap that determines how much you will receive per month. The length of the benefit payment (how long you will receive benefits) is also considered, as is the elimination period (the time you wait before benefits pay out. While a longer elimination period can potentially lower your costs a little, you have to self-insure for the elimination time – and this could mean needing months of cash savings. Other factors such as age, health, and lifestyle count too. Rely on a professional to help you structure your disability insurance, as these are rather complicated policies to set up.

Long-term disability insurance is available from agents, brokers, and directly from insurance companies. The advantage in using a broker is that they shop the market on your behalf to find the best policy for your unique situation. Brokers are compensated by insurance companies, but brokers are not tied to any one company. This means their services are free to you and they are free to work with as many different companies as possible to give you the best range of options.

|

Looking for a long-term disability insurance quote? Below are some factors that will be considered. Read them over then click the button below to get a quote.

|

Expert tip from Sean Borland “It is important if you are self-employed that you ensure your income that you are earning with disability insurance, your income that you are insuring has to be proven by providing ither a T4 or T1 form, your monthly benefit that you will receive from your Disability Insurance is roughly 65% of your gross annual income. There are a number of options to choose from with disability insurance that will impact the monthly premium that you will pay such as ” the waiting period ” which is the period of time that you choose before you start to receive your monthly benefit, the other is ” the benefit period” which is the period you will be receiving the monthly benefit for. There are also many other ” Riders” which are add On’s like future insurability, if you anticipate you are going to earn more in the future as a self employed individual you can show proof of your future earnings and increase the insured amount in the future. |

Looking for a long-term disability insurance quote? Below are some factors that will be considered. Read them over then click the button below to get a quote.

“It is important if you are self-employed that you ensure your income that you are earning with disability insurance, your income that you are insuring has to be proven by providing ither a T4 or T1 form, your monthly benefit that you will receive from your Disability Insurance is roughly 65% of your gross annual income.

There are a number of options to choose from with disability insurance that will impact the monthly premium that you will pay such as ” the waiting period ” which is the period of time that you choose before you start to receive your monthly benefit, the other is ” the benefit period” which is the period you will be receiving the monthly benefit for. There are also many other ” Riders” which are add On’s like future insurability, if you anticipate you are going to earn more in the future as a self employed individual you can show proof of your future earnings and increase the insured amount in the future.

Work with a broker to help reduce your chance of denial for long-term disability insurance. Since brokers work with a variety of carriers and have access to preview the applications, they know which policy is most likely to result in a successful outcome for you. If you do not qualify for traditional long-term disability coverage, your broker can discuss the other insurance options open to you.

Maternity leave is considered elective and therefore the leave itself is not covered by long-term disability insurance. However, depending on the policy, you may have coverage for unexpected complications arising from the pregnancy. For example, if the birth was difficult and your doctor does not clear you to go back to work within the time frame you and your employer expected, if you have medical complications from a C-section, or if you develop postpartum depression, there may be coverage under your long-term disability insurance plan. However, it is very important to note that each carrier treats long-term disability and pregnancy differently. Never assume about the coverage you have in place. If pregnant, or planning to be, talk with your broker or agent about what is covered under your plan, and fill in the gaps with extra coverage if needed.