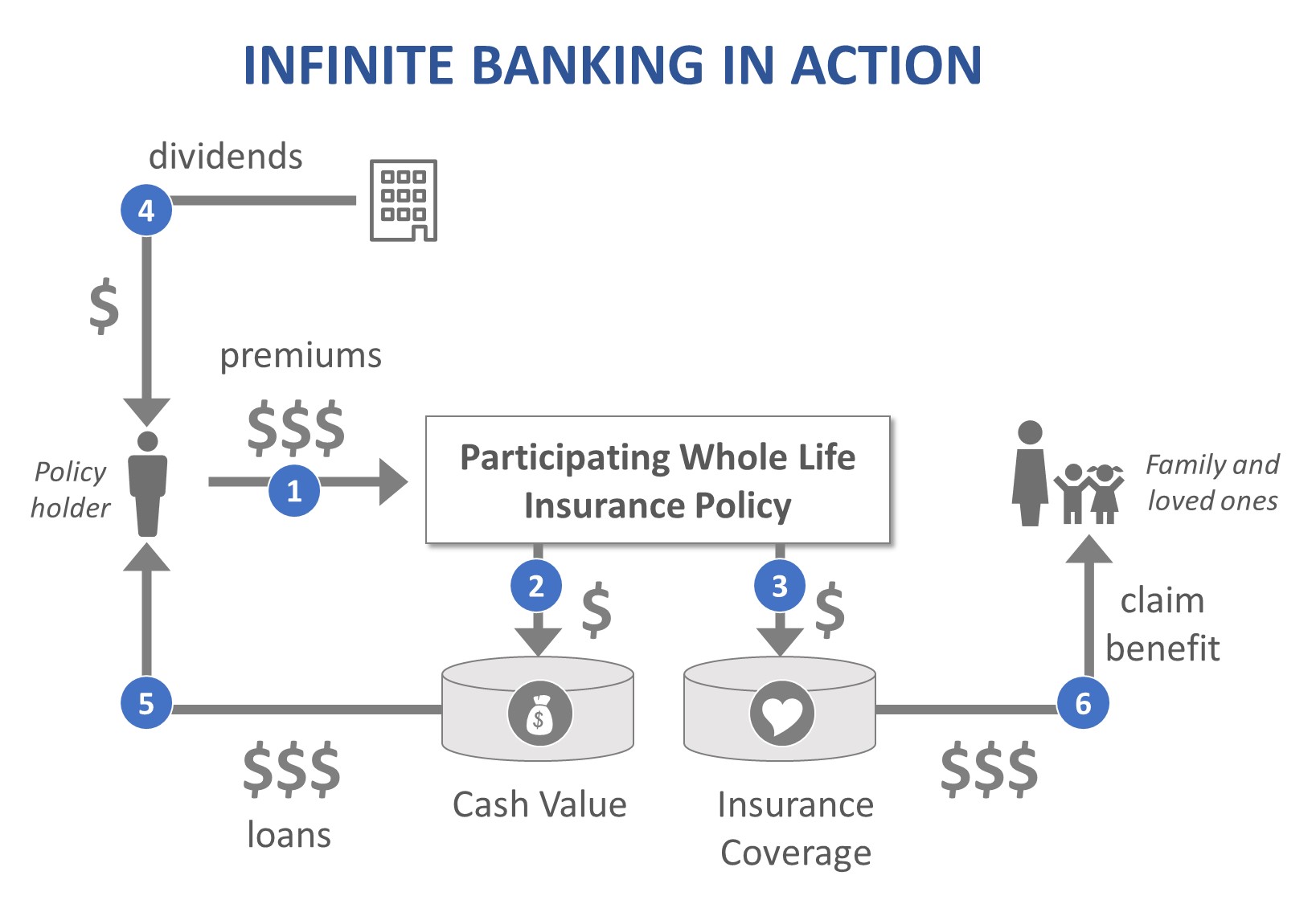

Infinite banking is a personal finance strategy that leverages a whole life policy as a “personal bank.” This includes taking loans against the policy and growing cash flow through the insurance’s dividends.

The core of the infinite banking concept is a participating whole life insurance policy. Once such a policy is in place, it is possible to lend yourself money using the cash value of the whole life insurance policy as collateral. That avoids paying interest to lending institutions since a policyholder has his/her own mini bank. It allows very fast access to extra funds, which are just an insurance company call away.

Typically, a participating whole life insurance policy is used for the infinite banking concept. Participating life insurance means that a policy pays dividends, which allow contribution towards the cash value of the policy or to pay a part of insurance premiums.

A simple visual below highlights the key elements of the infinite banking concept.

In order to start infinite banking, you need to work with a life insurance broker who has access to a wide range of whole life insurance policies and can choose the best product for your needs (premium rate, coverage rate, ability to drive dividends). The insurance broker will develop a financial plan with a focus on infinite banking and assist you through all the steps of setting up the policy.

Setting up an Infinite Banking policy in Canada involves selecting a whole life insurance policy, funding it with premiums, and structuring it for cash value growth. This strategy allows policyholders to use the accumulated cash value as a financing source for various projects, such as investments, renovations, or retirement income.

For instance, consider Sarah, a 35-year-old professional. She sets up an Infinite Banking policy, paying $10,000 annually. When she needs funds for home renovations, she borrows $50,000 from her policy’s cash value, avoiding traditional bank loans and maintaining control over her assets.

While there is no strict minimum policy size, it is important to remember that this strategy usually works better for higher-income earners, and the premiums reflect that. It is also important to note that, as policy loans are taxable in Canada, you want to ensure you have the ability to obtain a collateral loan in the later years of the policy. Larger amounts of cash surrender value will usually give you a better chance of securing preferable rates with banks.

|

A number of wealthy people use this concept to grow multi-generational wealth. That is why the answer is yes, infinite banking works in the cases when a few critical requirements are in place. One of the critical requirements is the ability to get a proper whole life insurance policy at meaningful rates. If the rates are too high (e.g. due to your health pre-condition) the whole concept might not work. Another key requirement is to be already financially sound and have a solid stream of income because premiums for a whole life insurance policy of a meaningful size are not low. It is important that you are able to pay these premiums to maintain the policy in-force. In many cases, it is advisable to plan to put up to 10% of your income into the whole life insurance policy. It is also advisable to have a solid financial understanding of key financial aspects associated with infinite banking (e.g. how compound interest works, how dividends work as a part of a participating life insurance, etc.) and good financial discipline. |

Expert intro: Phyllis Hofseth Infinite Banking uses one of the oldest financial tools out there: Participating Whole Life Insurance. This method is best when utilizing the dividend option known as Paid Up Additions. With this option, when the Whole Life policy owner receives a dividend, it is used to purchase additional Whole Life Insurance. These additions are paid up, meaning there are no further payments required. As a result, both the death benefit and the cash value of the policy increase. The Infinite Banking Concept (IBC) works best with Participating Whole Life policies and does not require a minimum size policy, making it flexible for various financial situations. Both Mutual companies and publicly traded insurance companies can be used for IBC. In Canada, the two primary Mutual companies selling participating whole life insurance are Equitable Life and Assumption Life. |

A number of wealthy people use this concept to grow multi-generational wealth. That is why the answer is yes, infinite banking works in the cases when a few critical requirements are in place.

One of the critical requirements is the ability to get a proper whole life insurance policy at meaningful rates. If the rates are too high (e.g. due to your health pre-condition) the whole concept might not work.

Another key requirement is to be already financially sound and have a solid stream of income because premiums for a whole life insurance policy of a meaningful size are not low. It is important that you are able to pay these premiums to maintain the policy in-force. In many cases, it is advisable to plan to put up to 10% of your income into the whole life insurance policy.

It is also advisable to have a solid financial understanding of key financial aspects associated with infinite banking (e.g. how compound interest works, how dividends work as a part of a participating life insurance, etc.) and good financial discipline.

Infinite Banking uses one of the oldest financial tools out there: Participating Whole Life Insurance. This method is best when utilizing the dividend option known as Paid Up Additions. With this option, when the Whole Life policy owner receives a dividend, it is used to purchase additional Whole Life Insurance. These additions are paid up, meaning there are no further payments required. As a result, both the death benefit and the cash value of the policy increase.

The Infinite Banking Concept (IBC) works best with Participating Whole Life policies and does not require a minimum size policy, making it flexible for various financial situations. Both Mutual companies and publicly traded insurance companies can be used for IBC. In Canada, the two primary Mutual companies selling participating whole life insurance are Equitable Life and Assumption Life.

There are a number of pros and cons associated with infinite banking.

| Pros of infinite banking | Cons of infinite banking |

| Ability to have your “own bank” and lend money from it without paying interest to the 3rd party lenders. | Costs of a whole life insurance policy. |

| No need to go through a long lending process if you need a loan. | Not a good choice for those looking for short-term results as it takes years to accumulate a meaningful cash value to borrow against. |

| Ability to grow the cash value of a policy even faster with a participating whole life insurance policy that pays benefits. | Not a good choice for people who can not easily get access to a whole life insurance policy (e.g. due to health pre-conditions). |

| Ability to select unstructured payment instead of a predefined payment plan. | You need to have a very solid understanding of the infinite banking concept since there is a chance, because it is along-term strategy, that an advisor who set it up for you will not be there after several years. |

| Ability to transfer wealth across generations via the use of a participating whole life insurance. | The interest on a policy loan is typically more than the earnings. Remember that loans range from 8%-10% with returns ranging from 4%-6%. Each loan affects future earning potential. |

| Ability to benefit from an array of financial benefits e.g. lower interest rates, lack of market volatility, lack of penalty or late payment fees, etc. | Any policy loan in excess of the adjusted cost basis of the life insurance policy will be 100% taxable to the individual. |

| You continue accumulate interest on the entire cash value even if you borrowed against it. |

There are several aspects that matter when choosing the right infinite banking insurance policy.

First of all, it must be whole life insurance to ensure that the policy has both an insurance and cash accumulation component. It is against this cash accumulation component (cash value) that can lend money in future.

|

Secondly, it should be participating whole life insurance, meaning that you want it to pay regular dividends that will help your cash value to grow faster and/or you can use the dividends to pay a part of your insurance premium. Thirdly, it is advisable to use a life insurance policy from a mutual company. That means that policy holders become company owners. For example, Equitable Life, as a Canadian mutual company, has paid dividends constantly since 1936 without a single year interruption. Fourth, you want to determine the right size of a whole life insurance policy (coverage amount, etc.) based on your needs and on resulting life insurance premiums. That involves an understanding of the maximum amount that you are able to contribute to a life insurance policy on a regular basis. We recommend working with an experienced life insurance broker who understands the concept of infinite banking and has extensive experience with Canadian mutual life insurance companies and their whole life products. |

Expert tip from Steve Meldrum “Watch out for taxable policy loans. In Canada, there is the concept of ACB (Adjusted Costs Basis). The ACB diminishes over the lifespan of the policy due to various factors. As you take out policy loans, you accelerate grinding down the ACB dollar for dollar. After the ACB hits zero, policy loans become taxable. Those policy gains are 100% taxable as income. Do not get fooled by a free lunch in Canada. The US does not have the concept of ACB, so taking out policy loans there does not trigger tax the same way.” |

Choosing a mutual insurance company over a public insurance company for setting up an Infinite Banking concept (IBC) can offer advantages such as a customer-centric approach and potentially better policy terms, like higher dividends and lower premiums. Mutual insurers, owned by policyholders, often prioritize stability and long-term satisfaction. In contrast, public insurers, accountable to shareholders, may prioritize profit motives, potentially resulting in higher costs or less favorable terms.

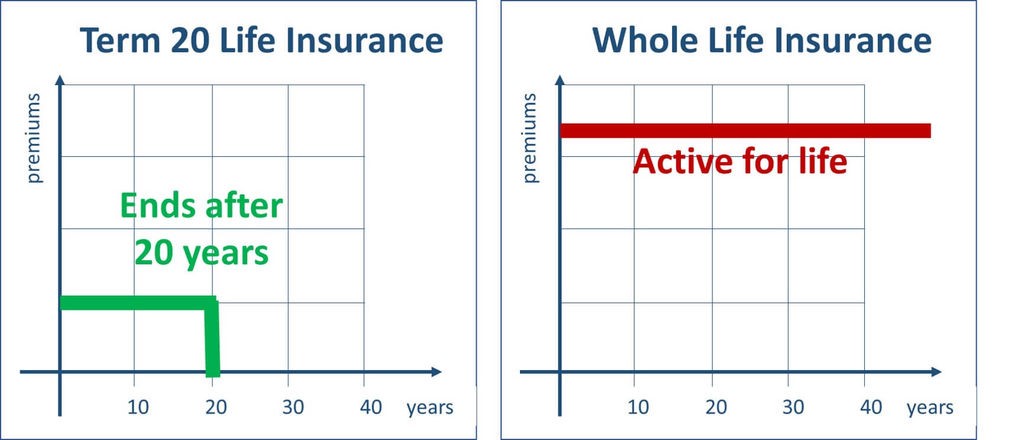

To truly understand the ins and outs of infinite banking, let’s first learn about whole life insurance and what makes it different from term life insurance.

Whole life insurance is a form of permanent insurance. As long as the premiums are paid, it does not expire. It also comes with a savings component – part of your premium goes into a cash savings account that accumulates value over time. You can receive the cash when you surrender the policy, use it to enhance the policy, or borrow against the cash.

Since whole life insurance is permanent, it presents greater risk for the insurer. Therefore, it has a higher premium than term. However, when one balances the fact of this against the fact that term insurance gets increasingly more expensive as one ages, and term doesn’t come with cash savings, the value of whole life insurance is clear.

Within the whole life insurance sphere, there are two variations: participating and non-participating insurance. Participating policies return dividends to the policy holder that can be used to pay your premiums or increase the amount of the benefit. This is why participating policies work so well for infinite banking. Note, however, that participating policies are typically more expensive than non-participating, and that dividends are not guaranteed.

Whole life insurance is uniquely positioned for infinite banking because it combines two sub-components. The investment component protects policy beneficiaries should you pass away. The cash accumulation components allow you to generate cash value the longer you hold the policy. Once the cash value is meaningfully high, you can borrow against the cash value and start enjoying all the benefits of infinite banking. The best thing is, even if you leverage your cash value, you will continue getting interest on the entire cash value. Ideally you would choose a participating whole life insurance policy so you can benefit from regular insurance dividends paid by an insurance company.The “Paid-Up Additions” (PUA) Whole Life Dividend option is recommended. This option maximizes the policy’s cash value growth and death benefit by using dividends to purchase additional coverage, which also earns dividends.

While Participating Whole Life Insurance is the preferred choice due to its guaranteed cash value growth and dividends, other types of life insurance, such as Universal Life can also be used. However, these alternatives generally lack the same level of guarantees and dividend potential, making them less ideal for this strategy.

|

We highly suggest getting infinite banking policies only from a mutual life company, meaning the dividend-paying participating policy holders actually own the company. An example of a Canadian mutual life insurance company is Equitable Life, whose policy is a great option for an infinite banking concept. Equitable Life is the largest mutual life insurer in Canada. There are a number of other Canadian life insurance companies that provide a good structure for a participating whole life insurance policy for infinite banking. Examples include Manulife, Sun Life and Canada Life. The main difference between mutual and non-mutual companies is who owns the company.

The divisible surplus distributed is also known as dividends. In a mutual company, the sole beneficiaries are the participating policy owners. In a demutualized (or stock) company, the beneficiaries also include stockholders. |

Expert tip from Philip Setter “Infinite banking at its core is a methodology to rethink your banking and investing mindset to allow for significant wealth building throughout your lifetime and into the next generation. Through the use of whole life insurance with cash value, we can begin to build a wealth system. We can use this system to continuously grow the “value” while also using it to invest in other projects or leverage it for traditional loans taken such as vehicles, education, or housing. For the right person, this can be an excellent wealth-building strategy that when used properly can significantly increase the family’s wealth for generations to come. However, there are many complexities involved in this strategy that can be its downfall especially for lower to middle-income earners that have many financial uncertainties in their life. There is a high degree of commitment and discipline that is required to make this strategy effective…” |

Choosing a mutual insurance company over a public insurance company for setting up an Infinite Banking concept (IBC) can offer advantages such as a customer-centric approach and potentially better policy terms, like higher dividends and lower premiums. Mutual insurers, owned by policyholders, often prioritize stability and long-term satisfaction. In contrast, public insurers, accountable to shareholders, may prioritize profit motives, potentially resulting in higher costs or less favorable terms.

The Infinite Banking Concept (IBC) may not be a good option for the following individuals:

It is important to carefully evaluate your financial situation, goals, and comfort level with the complexities of Infinite Banking Concept before deciding if it is the right strategy for you. Consulting with a financial advisor can also help determine if Infinite Banking Concept is a suitable option.

Infinite banking concept originated in the United States and, you might be asking yourself “does infinite banking work in Canada?”

The answer is yes, however, know that in Canada policy loans are taxable above the adjusted cost base (ACB). We cannot stress this enough – work with a financial advisor to set up infinite banking properly. Failure to do so can have a heavy tax burden that reduces the potential of the desired outcome.

Setting up an Infinite Banking policy in Canada involves selecting a whole life insurance policy, funding it with premiums, and structuring it for cash value growth. This strategy allows policyholders to use the accumulated cash value as a financing source for various projects, such as investments, renovations, or retirement income.

For instance, consider Sarah, a 35-year-old professional. She sets up an Infinite Banking policy, paying $10,000 annually. When she needs funds for home renovations, she borrows $50,000 from her policy’s cash value, avoiding traditional bank loans and maintaining control over her assets.

While there is no strict minimum policy size, it is important to remember that this strategy usually works better for higher-income earners, and the premiums reflect that. It is also important to note that, as policy loans are taxable in Canada, you want to ensure you have the ability to obtain a collateral loan in the later years of the policy. Larger amounts of cash surrender value will usually give you a better chance of securing preferable rates with banks.

The main difference between setting up an IBC in Canada versus the United States lies in the tax treatment and regulations.

In Canada, policy loans generally aren’t taxable in the early years of a policy, providing tax-efficient access to the policy’s cash value. However, these loans can become taxable in later years due to the fact that the policy’s adjusted cost basis (ACB) starts to decrease. However, you can use collateral loans from a bank that are not taxable, though this option involves additional qualifying criteria that need to be considered.

In contrast, policy loans in the United States are typically not taxable, allowing for consistent tax-efficient access to the cash value throughout the life of the policy.

The tax advantages of IBC in Canada include tax-deferred growth of the policy’s cash value, meaning you don’t pay taxes on the gains as they accumulate. Additionally, policy loans generally aren’t taxable in the early years of a policy, providing tax-efficient access to funds. Additionally, the death benefit is paid out tax-free to beneficiaries, making IBC a tax-efficient strategy for wealth building and estate planning.

|

These insights have been shared by Philip Setter, an insurance and investment professional based out of Calgary, Alberta. Find out more about Philip here. There are six important things to watch out when considering infinite banking as one of your strategies:

|

Expert intro: Glen Zacher Glen and Margaret Zacher founded McGuire Financial and they have developed a very unique approach to helping people Find Money that they are currently losing unknowingly & unnecessarily. Glen has coached many of the top Advisors in Canada, giving them the necessary tools to succeed in their careers. Glen hosts the “Talk to the Experts” – AB #1 Talk Radio show. He has been heard on radio in Edmonton, Calgary, Kelowna, Toronto. Glen has been featured on the Corus Radio Network, 630Ched, NewsTalk 770, Shine105.9, AM1150, TheBear, 640AMGlobalNews, TSN1260AM, & Equitable Life of Canada. Glen regularly appears as a speaker “The Wealthy Entrepreneur” seminar for Doctors, Chiropractors, Dentists & Business Owners. Glen is a Certified Financial Planner (since 2000) and has received high honours from Canada’s Top Investment & Insurance companies, also rated as Top Three Best Financial Services in Edmonton. The book “The Bankers’ Secret,” co-authored by Glen Zacher and Jayson Lowe, provides financial tips and strategies for retirement planning, recapturing the interest on big loans, and becoming your own banker. Glen is a member of FP Canada & Million Dollar RoundTable (Top of the Table Member). Glen attends several coaching & educational events – Strategic Coach, Circle of Wealth, Glazer Kennedy, Training Business Pro’s, Elite MM, Coach Blueprint, AICPA, IDCWIN, etc. Glen leads the industry with public educational events, recently – Retirement Ready or Not – as well SuperConference, Ultimate Wealth Day have featured guest speakers – R Nelson Nash, Robert (Bob) Shiels, Robert Murphy, Paul Tobey, Brent Kesler, Mark Guthrie & Mike Riley. |

These insights have been shared by Philip Setter, an insurance and investment professional based out of Calgary, Alberta. Find out more about Philip here.

There are six important things to watch out when considering infinite banking as one of your strategies:

Glen and Margaret Zacher founded McGuire Financial and they have developed a very unique approach to helping people Find Money that they are currently losing unknowingly & unnecessarily.

Glen has coached many of the top Advisors in Canada, giving them the necessary tools to succeed in their careers.

Glen hosts the “Talk to the Experts” – AB #1 Talk Radio show. He has been heard on radio in Edmonton, Calgary, Kelowna, Toronto. Glen has been featured on the Corus Radio Network, 630Ched, NewsTalk 770, Shine105.9, AM1150, TheBear, 640AMGlobalNews, TSN1260AM, & Equitable Life of Canada. Glen regularly appears as a speaker “The Wealthy Entrepreneur” seminar for Doctors, Chiropractors, Dentists & Business Owners.

Glen is a Certified Financial Planner (since 2000) and has received high honours from Canada’s Top Investment & Insurance companies, also rated as Top Three Best Financial Services in Edmonton.

The book “The Bankers’ Secret,” co-authored by Glen Zacher and Jayson Lowe, provides financial tips and strategies for retirement planning, recapturing the interest on big loans, and becoming your own banker.

Glen is a member of FP Canada & Million Dollar RoundTable (Top of the Table Member). Glen attends several coaching & educational events – Strategic Coach, Circle of Wealth, Glazer Kennedy,

Training Business Pro’s, Elite MM, Coach Blueprint, AICPA, IDCWIN, etc.

Glen leads the industry with public educational events, recently – Retirement Ready or Not – as well SuperConference, Ultimate Wealth Day have featured guest speakers – R Nelson Nash, Robert (Bob) Shiels, Robert Murphy, Paul Tobey, Brent Kesler, Mark Guthrie & Mike Riley.

Choosing the right infinite banking agent or broker is extremely important as this person should have several characteristics:

Several of our insurance brokers check the boxes in all these categories and have assisted numerous Canadians who decided to become their own bankers and benefit from the infinite banking concept.

The infinite banking concept was formulated by Nelson Nash, a life insurance agent with 35 years’ experience. Nash was born in Greene County, Georgia. He started in the forestry industry and followed that with long-term military service, before he joined in the life insurance industry. Today, his son-in-law, David Stearns serves on the board of the Nelson Nash Institute after having taken over the leadership from Nelson in 2009.