Disability insurance is a type of insurance that substitutes part of your income should you become disabled. Unlike other forms of insurance, disability benefits do not come as a lump sum, but as monthly payouts.

Disability cases are clearly defined in an insurance policy and have a number of special conditions defining waiting times (elimination period), the types of work in which you can be engaged after disability, and much more.

Disability is one of the insurance coverages that you always need if you have a stream of income, and especially if people, such as your family members, rely on this income.

Here are a few things to know

Here is a brief comparison to show how disability insurance compares to critical illness insurance.

| Critical Illness Insurance | Disability Insurance | |

|---|---|---|

| Purpose | Lump sum that can be used in any way the beneficiary wants | Covers part of the beneficiary’s lost income due to a disability |

| Coverage Payout | One time lump sum | Regular monthly payments |

| Stackable | Yes | No |

Disability insurance rates are determined through numerous aspects, such as:

Disability insurance costs are higher than term life insurance costs.

Here are some examples for disability insurance cost. These disability insurance rates have been generated in September 2021.

Please note that these rates consider 90-day elimination period, benefit period to age 65, and job category 3A (most “white collar” workers: office, clerical, or light sales work with no manual duties), which is one of the most popular job categories.

| Scenario 1 | Scenario 2 | Scenario 3 | |

| Monthly benefit amount | $2,500 | $5,000 | $7,500 |

| Minimum annual income to qualify | $41,000 | $94,000 | $168,000 |

| Benefit, percentage of income | 73% | 64% | 54% |

| Female, age 30 | $91/month | $176/month | $263/month |

| Female, age 40 | $125/month | $245/month | $364/month |

| Female, age 50 | $159/month | $313/month | $468/month |

| Male, age 30 | $56/month | $107/month | $156/month |

| Male, age 40 | $83/month | $163/month | $239 /month |

| Male, age 50 | $135/month | $262/month | $394/month |

Source: Disability Insurance data from 2024.

The Disability Insurance Elimination Period is the waiting period between when an

individual becomes disabled and when they can start receiving disability benefits.

Common elimination periods are 30, 60, or 90 days. During this time, the policyholder is

responsible for covering their expenses independently, using personal savings,

employer benefits like sick leave, or other income sources, until the insurance benefits

kick in. The length of the elimination period typically impacts the cost of

premiums—longer waiting periods result in lower premiums.

The amount of disability insurance you need depends on your income, expenses, and

financial planning. It’s important to understand that part or all of your income may not be

available during a disability, and your disability insurance payments should be sufficient

to replace this income. Keep in mind that no policy covers 100% of your existing

income—typically, benefits are capped at 60-80% of your pre-accident income. In some

cases, policies may cover up to 75%. This cap ensures you still have the motivation to

recover. Additionally, you cannot combine two policies that each cover 75% of your

income to receive 150% in benefits.

Disability insurance is not required by law in Canada, but it is highly recommended for

individuals to protect their income in the event of illness or injury. While Employment

Insurance (EI) Sickness Benefits provide temporary support, disability insurance works

in conjunction with these benefits, as well as group disability coverage offered by

employers, to offer more comprehensive financial protection.

In addition to voluntary coverage, there are specific situations where disability insurance

is mandatory.

For instance, Workers’ Compensation Insurance, provided through organizations like

the Workplace Safety and Insurance Board (WSIB) in Ontario, is required by law for

many types of jobs in Canada. However, the responsibility for securing this coverage

falls on the employer, not the employee.

Furthermore, in certain high-risk activities, such as martial arts competitions,

participants may be required to provide proof of disability or accident insurance

coverage before being allowed to compete. This ensures that individuals are financially

protected in case of an injury, and it is a condition for participation in these events.

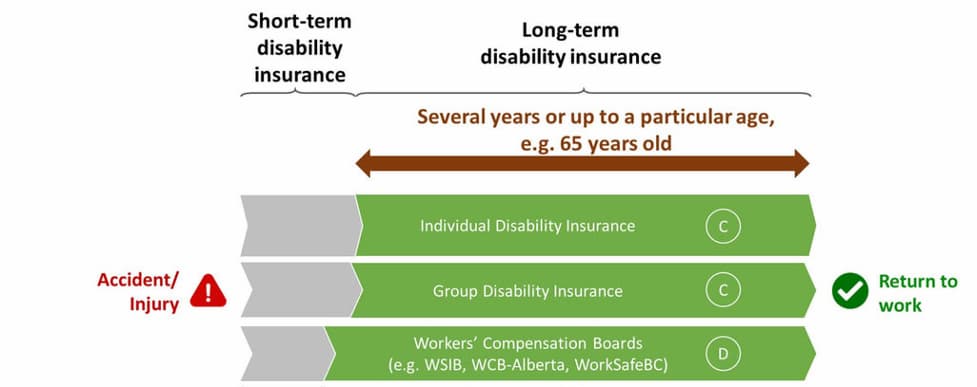

There are two types of disability insurance: short-term and long-term.

Short-term disability typically lasts for about six months, and if necessary, long-term

disability coverage can begin once short-term benefits run out.

Long-term disability insurance is available to individuals through group benefits (such

as those provided by employers or associations) or through Workers’ Compensation

Board (WSIB) coverage. In some cases, long-term disability coverage can last for

years, or even until retirement.

Long-term disability kicks in once short-term coverage ends, usually after about six

months. It can be provided through an individual policy, a group policy, or through

Workers’ Compensation Board coverage like WSIB.

The duration of long-term disability benefits typically falls into three categories: until you

can return to work, until you reach a certain age (often 65), or until a specified maximum

year limit (e.g., five years). These limits vary by insurer and policy.