Life insurance types by coverage length: Term vs Permanent

Life Insurance type by ability to generate cash: Term 100 vs Whole Life vs Universal Life

Life Insurance types based on ease to get: Fully underwritten vs No Medical Life Insurance

Life Insurance types based on ability to pay dividends: Participating vs Non-Participating

Life Insurance types based on ownership: Individual Life vs Corporate-owned Life

Life Insurance type by reason: Standard Life vs Mortgage Life vs Accident Life

Life Insurance type by person covered: Individual Life vs Multi-Life vs Joint Life Insurance

Life Insurance type based on beneficiary: Revocable vs Irrevocable Beneficiary

Life insurance is one of the oldest and most established financial products, designed to provide peace of mind and financial security for loved ones. Over time, it has evolved significantly, leading to the creation of various types of life insurance tailored to different needs and situations. While some options are straightforward, others can be complex and may require guidance from an experienced insurance professional. To help you navigate this landscape, we’ve developed one of the most comprehensive yet simple overviews of life insurance types. There are several ways to classify these products—let’s begin.

The first and simplest way to categorize life insurance types is based on the policy’s duration: either for a pre-determined timeframe, typically measured in years, or for the lifetime of the policyholder (i.e., permanent coverage, as long as premiums are paid). That’s why the names: Term Life Insurance and Permanent Life Insurance.

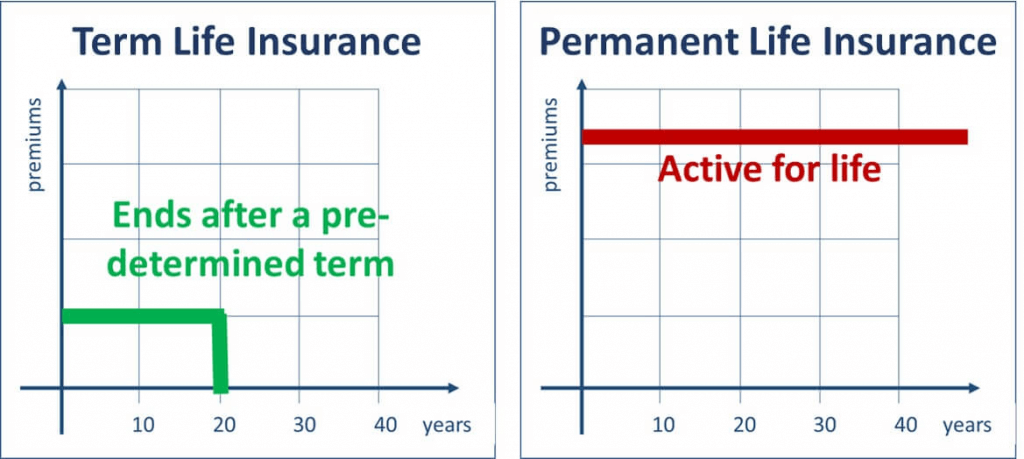

Term Life Insurance policies are designed to cover short-term needs and are the simplest form of life insurance. They provide the largest benefit for the lowest initial premium. The benefits from this coverage can be used to pay off debt or meet other financial needs. While premiums start low, they increase as the insured ages. Term policies typically last for 10, 20, or 30 years, though some providers also offer options like Term 40.

This type of life insurance provides coverage until the policy matures, as long as the insured pays the premiums on time. The four major types of permanent insurance are Whole Life, Universal Life, and Term 100. We will explore these in more detail in the next chapter.

So, in a nutshell, the comparison of these two life insurance types looks as follows:

| Criteria | Term Life Insurance Type | Permanent Life Insurance Type |

| Coverage Duration | Coverage for a specified term (e.g., 10, 20, 30 years) | Coverage for the insured’s entire lifetime |

| Premiums | Lower initially, but increase upon renewal | Typically higher, but fixed or level over time |

| Cash Value | No cash value accumulation | Some types can accumulate cash value over time |

| Renewability | Renewable at the end of the term (with higher premiums) | Non-renewable, as coverage is for life |

| Purpose | Ideal for short-term financial needs (e.g., mortgage, income replacement) | Ideal for long-term needs (e.g., estate planning, lifelong coverage) |

Permanent life insurance provides lifelong coverage as long as premiums are paid, offering a combination of insurance protection and, in some cases, a cash value component that grows over time. It includes various types, such as Whole Life and Universal Life, which often involve savings or investment elements.

Term 100, while technically a type of permanent insurance, is distinct in that it provides lifetime coverage but has no cash value accumulation.

Now let’s dive deeper…

Whole Life Insurance policies give lifetime coverage as long as the premiums are paid on time. The premiums stay the same throughout the policy, and the plan also builds cash value over time. You can borrow against this cash value.

Universal Life Insurance offers flexible premiums and adjustable benefits. The policyholder can change the amount of coverage based on their needs. These policies can provide either a fixed death benefit or one that increases over time, with options for either a rising cost of insurance or a level cost.

Term 100 (also called Term to 100) Life Insurance provides lifetime coverage as long as you continue to pay the premiums, which stay the same throughout your life. If you reach age 100, the insurance company will continue coverage, but you won’t have to pay premiums anymore.

The main difference between Term 100 and Whole Life insurance is that Term 100 offers level premiums and lifetime protection, but it doesn’t build cash value like participating Whole Life policies do.

So, in a nutshell, the comparison of these life insurance types looks as follows:

| Criteria | Term 100 Insurance Type | Whole Life Insurance Type | Universal Life Insurance Type |

|---|---|---|---|

| Coverage Duration | Lifetime coverage as long as premiums are paid | ||

| Premiums | Level premiums throughout the policy | Flexible premiums, can be adjusted over time | |

| Cash Value | No cash value | Builds cash value over time | Builds cash value, can be adjusted with premiums |

| Loans Against Policy | No loan option | Loans can be taken against the cash value | |

| Death Benefit | Fixed death benefit | Flexible death benefit (can be adjusted) | |

| Premium Adjustments | No adjustments, premiums stay the same | Premiums can be adjusted based on the policyholder’s needs | |

| Cash Value Growth | N/A | Guaranteed and potential non-guaranteed growth | Non-guaranteed cash value growth, depends on interest rates and policy performance |

| Dividends | None | May offer dividends in participating policies | No dividends |

| Flexibility | Limited flexibility | High flexibility in premiums and death benefit | |

| Purpose | Those looking for affordable lifelong coverage | Those seeking guaranteed lifelong coverage with cash value | Those looking for flexibility in premiums and death benefit |

Fully Underwritten Life Insurance policies with a medical exam require the policyholder to undergo a comprehensive medical evaluation. This process involves providing health history, undergoing a physical exam, and sometimes additional tests (e.g., blood and urine tests). The insurer uses this information to assess the applicant’s health risks and determine the premium rate. This type of life insurance generally offers higher coverage amounts and lower premiums compared to other options because it provides the insurer with a thorough understanding of the applicant’s health.

Fully Underwritten Life Insurance policies without a medical exam still require the applicant to answer detailed health questions and disclose medical history. However, instead of undergoing a medical exam, the insurer typically relies on the answers provided by the applicant, along with other data sources like prescription history or previous medical records, to assess the risk. This type of insurance is typically reserved for relatively healthy individuals without major health pre-conditions, who are young or in their 40s, and is generally not available for more senior applicants.

No Medical Life Insurance is a type of policy that doesn’t require a medical exam or extensive health questionnaires. It is typically easier and faster to qualify for, making it an attractive option for those who may have health issues or don’t want to go through the underwriting process. However, because the insurer takes on more risk without knowing the applicant’s health status, these policies usually come with higher premiums and lower coverage amounts than fully underwritten policies. There are two main sub-types of policies in this category: Guaranteed Issue and Simplified Issue policies.

Simplified Issue Life Insurance Policies represent a type of life insurance that requires the applicant to answer a few health-related questions, but does not require a medical exam. It is a faster and easier way to get coverage, though premiums may be higher than fully underwritten policies due to the limited health information available.

Guaranteed Issue Life Insurance Policies offer life insurance without requiring any health questions or medical exams, ensuring acceptance for all applicants within a certain age range. While it provides easy access to coverage, these policies typically come with higher premiums and lower death benefits, and may have a waiting period (typically, two years) before the full benefit is payable.

So, in a nutshell, the comparison of these life insurance types looks as follows:

| Criteria | Fully Underwritten with Medical Exam | Fully Underwritten without Medical Exam | No Medical Life Insurance (Simplified Issue) | No Medical Life Insurance (Guaranteed Issue) |

| Medical Exam Required | Yes | No | ||

| Health Questions | Detailed health history required | Limited health questions | No health questions | |

| Coverage Amount | Typically high (up to millions) | Typically high (but may be lower than fully underwritten) | Moderate to high | Typically lower |

| Premiums | Generally lower compared to no-medical options | Higher than with a medical exam | Higher than fully underwritten policies | Highest premiums due to guaranteed acceptance |

| Approval Process | Longer (weeks to months) | Moderate (a few weeks) | Fast (days to a week) | Very fast (usually within a few days) |

| Risk to Insurer | Lower risk, as health status is fully assessed | Moderate risk, based on applicant’s self-report | Higher risk, as health is not fully disclosed | Highest risk, as no health information is provided |

| Typical Applicants | Healthy individuals in good health | Healthy individuals, but no medical exam required | Those who need fast approval or have mild health issues | Those with serious health concerns or who cannot qualify for other options |

| Policy Availability for Seniors | Available, but premiums increase with age | Not typically available for seniors (age limits) | Available for seniors, but with higher premiums | |

Participating life insurance policies offer the potential for dividends, which are based on the insurer’s financial performance and can be used to reduce premiums, purchase additional coverage, or be paid out in cash. While these dividends are not guaranteed, they provide the opportunity for policyholders to share in the insurer’s profits.

There are several options available for a policyholder to choose from when it comes to their dividends. These options include:

In contrast, non-participating policies do not offer dividends, providing a fixed premium and guaranteed death benefit. They are more predictable and generally less expensive, but lack the potential for additional value through dividends.

Participating whole life insurance is likely the best option for those who want their cash values to grow and compound on a tax-deferred basis. However, dividend interest rates can fluctuate from year to year, and there is no guarantee that the life insurance company will pay dividends.

So, in a nutshell, the comparison of these life insurance types looks as follows:

| Criteria | Participating Life Insurance | Non-Participating Life Insurance |

| Dividends | Potential for dividends based on the insurer’s financial performance | No dividends paid to policyholder |

| Premiums | Premiums may be higher due to potential for dividends | Typically, lower and fixed premiums |

| Death Benefit | Guaranteed death benefit plus potential growth from dividends | Guaranteed death benefit |

| Cash Value | Builds cash value, which may increase with dividends | Builds cash value, but no dividends to boost growth |

| Flexibility | Flexible use of dividends (e.g., premium reduction, cash payouts, paid-up additions) | No dividends or flexibility for policy growth |

| Predictability | Less predictable due to dividend variability | More predictable, with fixed premiums and benefits |

Individual life insurance is purchased by a person to provide financial protection for their beneficiaries in case of death. The policyholder owns the policy, controls premiums and coverage, and customizes it based on personal needs such as income replacement, debt, and estate planning. Premiums are determined by the individual’s health and lifestyle.

Corporate-owned life insurance (COLI), on the other hand, is purchased by a company to insure key employees or executives. The company owns the policy, pays the premiums, and is the beneficiary. The death benefit is used for business needs like covering the loss of key personnel, paying off debts, or funding buy-sell agreements. COLI can also build tax-deferred cash value for the business.

So, in a nutshell, the comparison of these two life insurance types looks as follows:

| Criteria | Individual Life Insurance | Corporate-Owned Life Insurance (COLI) |

| Policy Ownership | Owned by the individual | Owned by the business |

| Premium Payments | Paid by the individual | Paid by the company |

| Beneficiaries | Designated by the policyholder (usually family or loved ones) | The business itself is the beneficiary |

| Purpose | Personal financial protection (income replacement, estate planning) | Business continuity, covering key employees, or buy-sell agreements |

| Control | Full control over the policy (premiums, beneficiary, etc.) | The business controls the policy and how the death benefit is used |

| Tax Treatment | Death benefit is generally tax-free to beneficiaries | Death benefit is typically tax-free to the company, with potential tax advantages for cash value growth |

Life insurance can be categorized based on the specific reason or need for the coverage. Standard Life Insurance provides general coverage for individuals, offering financial protection for dependents or beneficiaries in the event of the policyholder’s death. It can be used to cover a wide range of needs, such as income replacement, debt repayment, or estate planning. Mortgage Life Insurance is designed to pay off the remaining balance of a mortgage if the policyholder passes away. This ensures that the family or beneficiaries are not burdened with mortgage debt. Accident Life Insurance offers coverage specifically in the event of death caused by an accident. It is a more specialized form of life insurance.

So, in a nutshell, the comparison of these life insurance types looks as follows:

| Criteria | Standard Life Insurance Type | Mortgage Life Insurance Type | Accident Life Insurance Type |

| Typical use for… | Those seeking comprehensive life insurance | Homeowners with a mortgage | Individuals with higher accident risks or seeking additional coverage |

| Coverage | Death by any cause | Pays off mortgage debt if the policyholder passes away | Pays out only if death is accidental |

| Purpose | General financial protection for beneficiaries | To cover the outstanding mortgage balance upon death | Provides coverage in case of accidental death |

Individual Life Insurance is a policy where one person is covered for life, paying premiums to provide a death benefit for their beneficiaries. This type of insurance is ideal for individuals seeking personal financial protection and long-term security for their family. It can be customized to meet the policyholder’s needs, such as choosing the coverage amount, premium type, and additional riders.

Multi-Life Insurance, on the other hand, covers multiple individuals under a single policy, typically used by families, business partners, or groups. It can often offer discounted premiums for covering several lives in one plan, making it cost-effective.

Joint Life Insurance, a type of multi-life insurance, insures two people under one policy. There are two main types: Joint Life First-to-Die, which pays out when the first insured person passes away, and Joint Life Last-to-Die, which pays out only after both insured individuals have passed away. Joint life insurance is commonly used by married couples or business partners who want to ensure financial protection for their beneficiaries in the event of death.

So, in a nutshell, the comparison of these life insurance types looks as follows:

| Criteria | Individual Life Insurance Type | Multi-Life Insurance Type | Joint Life First-to-Die Insurance Type | Joint Life Last-to-Die Insurance Type |

| Coverage | Covers one individual | Covers multiple individuals under one policy | Covers two people, payout occurs when the first person passes | Covers two people, payout occurs after both individuals pass |

| Best for | Individuals seeking personal protection | Families, business partners, or groups looking for cost-effective coverage | Couples or business partners needing financial security for surviving beneficiaries | Estate planning or ensuring financial security for heirs |

| Purpose | Provides tailored financial protection | Offers coverage for several lives in one plan | Supports financial needs of the surviving partner or business continuity | Protects long-term family wealth or legacy goals |

| Cost | Premiums based on a single life | Potential discounts for insuring multiple lives | Often less expensive than two individual policies | Typically, more cost-effective for estate protection |

| Payout Timing | Upon the policyholder’s death | Upon death of each insured individual | Upon the death of the first insured person | Upon the death of the second insured person |

Life insurance beneficiaries can be either revocable or irrevocable, depending on how much control the policyholder wants. With a revocable beneficiary, the policyholder can change the beneficiary at any time without their permission, offering flexibility if circumstances change. An irrevocable beneficiary, however, cannot be changed without their consent, ensuring they are guaranteed the policy’s death benefit. Irrevocable beneficiaries are often used in situations like divorce agreements or business contracts to secure financial protection.

So, in a nutshell, the comparison of these two life insurance types looks as follows:

| Criteria | Life Insurance with Revocable Beneficiary | Life Insurance with Irrevocable Beneficiary |

| Ability to Change Beneficiary | Can be changed at any time without the beneficiary’s consent. | Cannot be changed without the beneficiary’s written consent. |

| Flexibility | Highly flexible for the policyholder. | Limited flexibility for the policyholder. |

| Guarantee to Beneficiary | No guarantee, as the beneficiary can be replaced. | Guaranteed right to the policy’s death benefit. |

| Common Use Cases | Personal policies where circumstances may change (e.g., marriage, children). | Legal agreements like divorce settlements or business contracts. |

| Legal or Financial Implications | Fewer restrictions; easier to manage. | May involve legal restrictions or obligations. |

There are many types of life insurance available, ranging from straightforward options to more complex policies that may require detailed explanations to fully understand. While some, like Term Life Insurance, are simple and easy to grasp, others, such as Universal Life or Participating Whole Life, involve features and benefits that might not be immediately clear. This is where guidance from an experienced insurance professional becomes invaluable. Our team of experts is here to help you navigate the options and find the life insurance policy that best suits your needs. Simply complete a quote on the sidebar to get started!